Getting your first credit card in the U.S. can feel overwhelming, especially when you come across terms like secured vs unsecured credit cards. At first, they may sound alike, but they work very differently—and the choice you make can directly affect how fast you build credit, how much interest you pay, and what financial options you unlock in the future.

If you’re just starting out, rebuilding a low score, or trying to qualify for better rates and rewards, understanding the difference between a secured credit card and an unsecured credit card is essential. A secured credit card requires a refundable deposit, which usually becomes your credit limit, making it easier to get approved. On the other hand, an unsecured credit card doesn’t require any upfront payment, but approval depends more on your credit history, income, and overall financial profile.

Your choice isn’t just about approval—it’s about building a strong financial future. Choosing the right secured vs unsecured credit card can help you minimize fees, manage interest wisely, and steadily improve your credit score over time. On the other hand, picking the wrong option could delay your credit-building journey and lead to unnecessary costs.

The good news? Both secured and unsecured credit cards can be powerful tools to build credit when used responsibly. By making on-time payments, keeping your balance low, and using your card wisely, you can strengthen your credit profile over time—no matter which option you choose.

In this 2026 guide, you’ll get a clear breakdown of secured vs unsecured credit cards, including their key differences, real benefits, and common mistakes to avoid—so you can confidently choose the card that fits your situation and start building better credit today.

Consumer Financial Protection Bureau – Credit Cards Guide

Table of Contents

What Is a Secured Credit Card?

What Is a Secured Credit Card (Experian Guide)

A secured credit card requires you to put down a refundable security deposit when you open the account. In most cases, this deposit acts as your credit limit—so if you deposit $300, that’s typically how much you can spend on the card.

This setup lowers the risk for the lender, which is why secured cards are much easier to get approved for in the U.S., especially if you have no credit history or a low credit score. Even though you’re using your own money as a backup, you still use the card just like a regular credit card—making purchases, paying your bill, and building your credit over time.

The best part is that your deposit isn’t lost. As long as you manage your account responsibly—like making on-time payments and keeping your balance low—you can often upgrade to an unsecured card later and get your full deposit back.

Key Features of Secured Credit Cards

- Requires upfront deposit ($200–$500)

- Easy approval for beginners

- Helps build credit history

- Lower risk of overspending

How It Works

- Deposit $300 → Credit limit = $300

- Use card for small purchases

- Pay bill on time every month

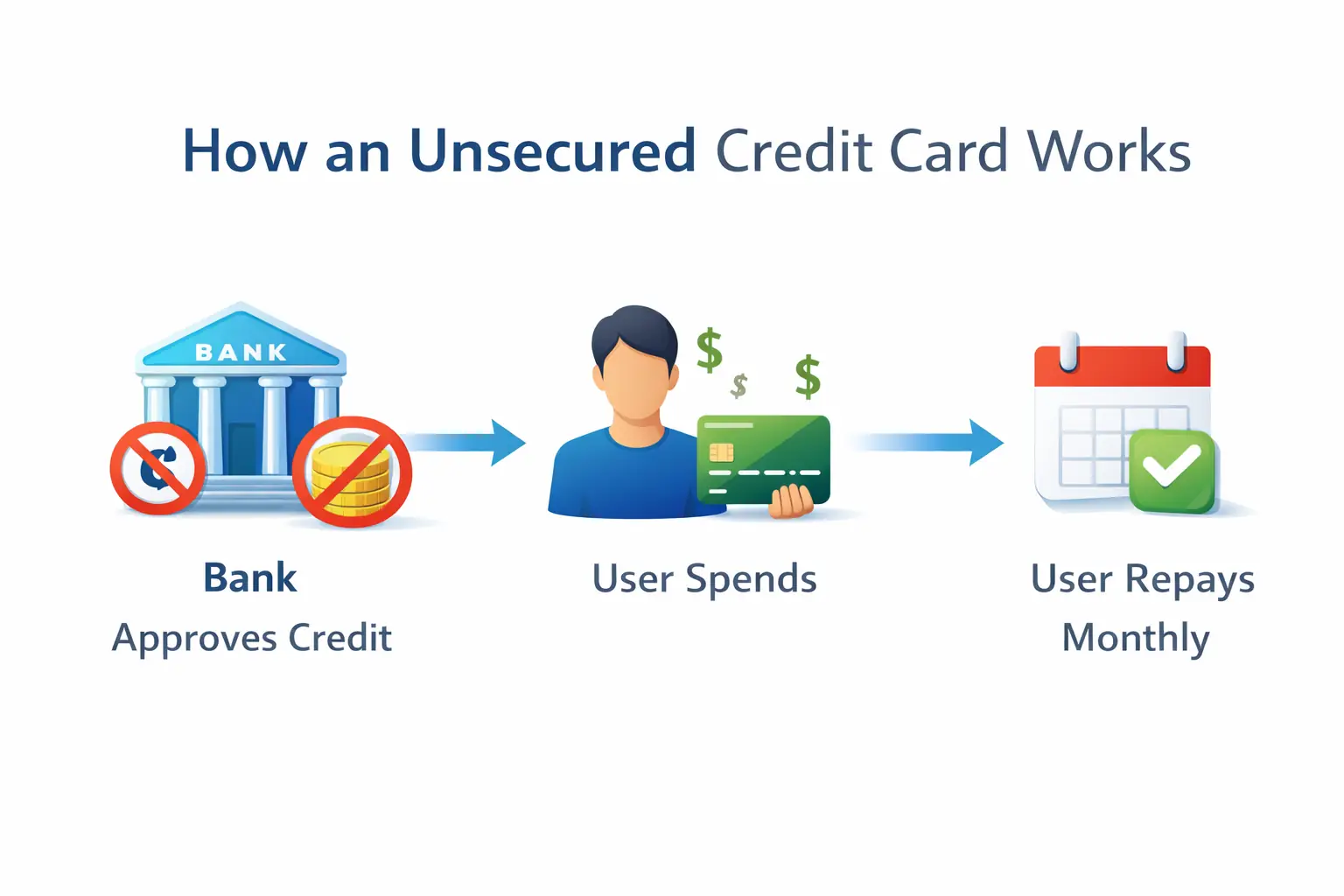

What Is an Unsecured Credit Card?

An unsecured credit card doesn’t require any upfront deposit to get started. Instead of asking for collateral, the card issuer approves you based on your creditworthiness—things like your credit score, income, payment history, and overall financial profile.

Because there’s no security deposit backing the account, lenders take on more risk. That’s why approval is usually easier if you already have a fair to good credit history. If you’re just starting out, you may still qualify for certain entry-level or student unsecured cards, but the terms—like lower credit limits or higher interest rates—can vary.

Once approved, you can use the card just like any standard credit card: make purchases, pay your bill each month, and build your credit over time. Responsible use, such as paying on time and keeping your balance low, can help you qualify for better cards with higher limits and rewards in the future.

Key Features of Unsecured Credit Cards

- No deposit required

- Higher credit limits

- Rewards and cashback

- Requires fair or good credit

How It Works

- Bank gives credit limit (e.g., $1,000)

- You spend and repay monthly

- If you don’t pay off your full balance, interest will be charged

Secured vs Unsecured Credit Cards for Beginners (Comparison Table)

| Feature | Secured Credit Card | Unsecured Credit Card |

|---|---|---|

| Deposit | Required | Not Required |

| Approval | Easy | Moderate/Hard |

| Credit Limit | Based on deposit | Based on credit score |

| Rewards | Limited | Available |

| Best For | No credit/bad credit | Fair/good credit |

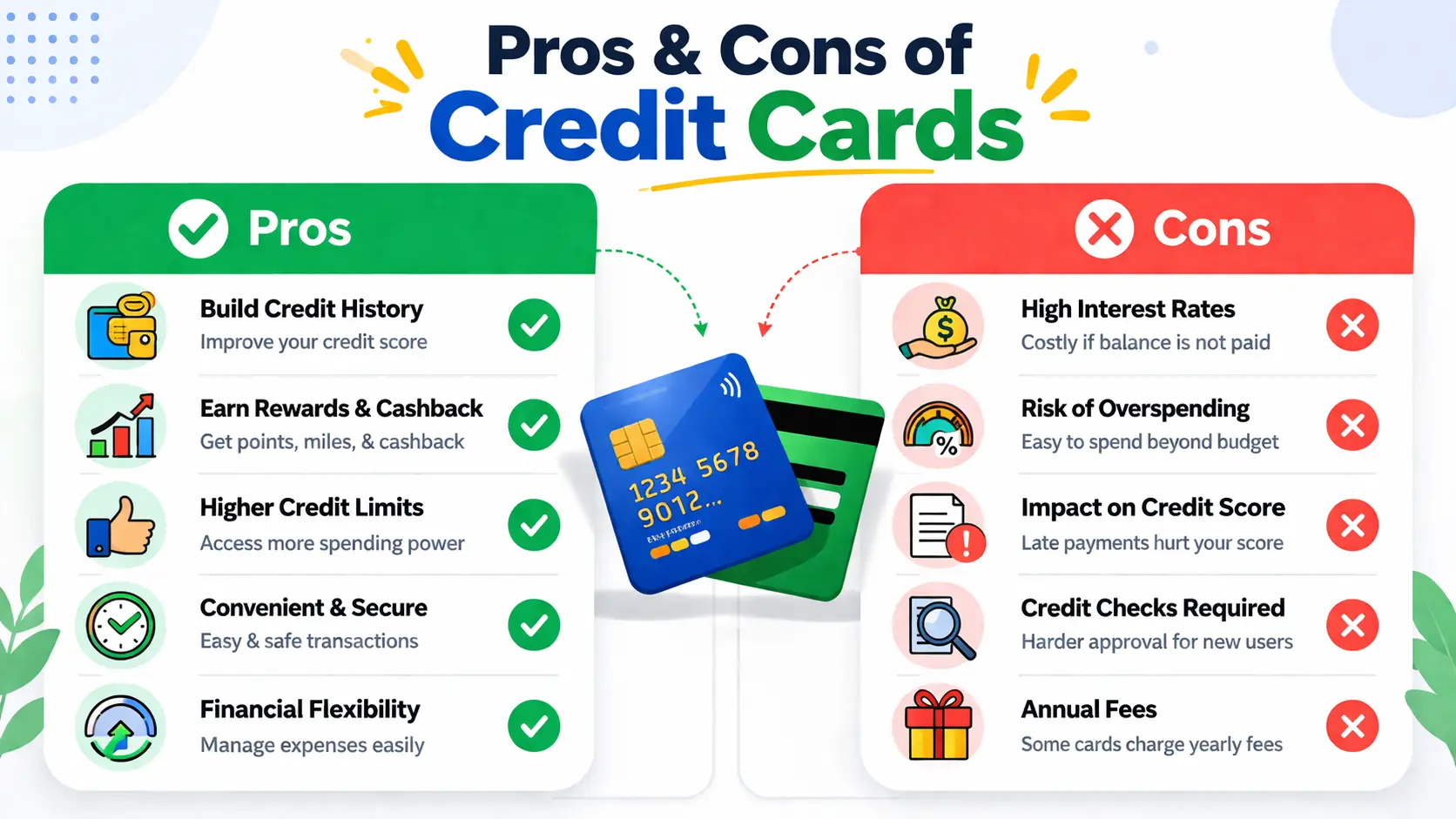

Pros and Cons of Secured Credit Cards

✅ Pros

- Easy approval

- Great for building credit

- Lower financial risk

- Upgrade option available

❌ Cons

- Requires deposit

- Low credit limit

- Fewer rewards

Pros and Cons of Unsecured Credit Cards Explained

✅ Pros

- No upfront deposit

- Higher limits

- Cashback and rewards

- Builds strong credit profile

❌ Cons

- Harder to get approved

- High interest rates

- Risk of overspending

Quick Difference List

Secured Credit Card:

- Best for beginners

- Needs deposit

- Safe option

Unsecured Credit Card:

- Best for experienced users

- No deposit

- More benefits

Example Scenario Table

| Situation | Best Choice |

|---|---|

| No credit history | Secured Card |

| Low credit score | Secured Card |

| Fair credit (650+) | Unsecured Card |

| Want rewards | Unsecured Card |

Who Should Use a Secured Credit Card?

- First-time credit users

- Students or beginners

- People with bad credit

- Those rebuilding credit

Who Should Use an Unsecured Credit Card?

- Users with fair/good credit

- People with stable income

- Those looking for rewards

- Experienced card users

Who Should Avoid Secured Credit Cards?

- If you can qualify for unsecured cards

- If you don’t want to lock money as deposit

Who Should Avoid Unsecured Credit Cards?

- Beginners with no credit

- People who overspend easily

- Those with poor credit history

How to Build Credit Fast (Beginner Tips)

- Pay bills on time (most important)

- Pay full balance every month

- Avoid multiple applications

- Keep your card active

Conclusion

Choosing between secured and unsecured credit cards ultimately comes down to your current credit situation and financial starting point. The right choice isn’t about which card is “better”—it’s about which one fits your needs today and helps you move forward with confidence.

- No credit or starting fresh? A secured credit card is usually the best place to begin. It’s easier to get approved, helps you build a positive payment history, and gives you a reliable path toward qualifying for better credit options in the future.

- Already have some credit history? An unsecured credit card may be a better fit. It doesn’t require a deposit and can offer more flexibility, along with opportunities to access higher limits and rewards as you continue to build your profile.

No matter which route you choose, the real impact comes from how you use your card. Consistently paying your bills on time, keeping your balances low, and managing your credit responsibly are the habits that truly make a difference.

Make a smart, informed decision based on where you stand today, stay disciplined with your usage, and you’ll be well on your way to building a stronger credit score throughout 2026 and beyond.

Key FAQs on Secured ad Unsecured Credit Cards Explained

Should I choose a secured or unsecured credit card for building credit?

Choose a secured credit card if you have no or poor credit, as it requires a deposit and is easier to get approved. If you have good credit, an unsecured credit card is better since it doesn’t require any deposit.

Secured vs unsecured credit card – what do people say on Reddit?

On Reddit, most users suggest starting with a secured credit card to build credit, then upgrading to an unsecured card after 6–12 months of responsible use.

What are the best unsecured credit cards?

Popular options include Discover it Cash Back Credit Card, Chase Freedom Unlimited, and Capital One Quicksilver Cash Rewards Credit Card. The best choice depends on your credit score and spending habits.

How can I apply for an unsecured credit card?

Check your credit score, compare cards, choose one that fits your profile, and apply online through the card issuer’s website. Approval depends on your creditworthiness.

What is a secured credit card?

A secured credit card requires a refundable deposit that becomes your credit limit. It helps people with no or bad credit build their credit history.

Are there unsecured credit cards for bad credit?

Yes, but they often come with higher fees and interest rates. Issuers like Capital One offer options, but secured cards are usually easier to get approved for.