The best credit card in the USA 2026 can be one of the most valuable tools in your financial journey when used wisely. Choosing the best credit card for your credit score allows you to build strong credit, earn cashback or travel rewards, and manage everyday expenses more efficiently. Many top credit cards in the USA also offer perks like purchase protection, travel benefits, and low introductory APR. However, if you misuse even the best rewards credit cards, it can lead to high-interest debt and financial stress, making it important to use your card responsibly.

Best credit card in the USA 2026 is not just about picking a popular name—it’s about choosing a card that truly matches your lifestyle, spending habits, and credit profile. The top credit cards in the USA offer a wide range of benefits, from cashback and travel rewards to low APR and premium perks. But with so many options available, finding the best credit card for your credit score can feel overwhelming. Many people rush the decision and end up choosing from the best rewards credit cards without fully understanding the terms, which can cost them more in the long run instead of maximizing value.

In this complete guide, you will learn everything step by step. We will break down how credit cards work, explain all major types of credit cards in detail, and help you choose the best option based on your credit score. You’ll also see real examples of top U.S. credit cards, understand their benefits, and learn how to apply successfully.

Whether you are a beginner with no credit, someone rebuilding your score, or an experienced user looking for premium rewards, this guide will help you make the right decision in 2026.

learn about credit cards from the CFPB

Table of Contents

What Is a Credit Card and How Does It Work?

A credit card is issued by a bank or financial institution that allows you to borrow money up to a certain limit. You can use this money to pay for goods and services, both online and offline.

Instead of paying immediately, you repay the borrowed amount later—either in full or over time.

Each month, your card provider sends a billing statement that includes:

- Total amount spent

- Minimum payment due

- Payment due date

When you pay off your entire balance by the due date, you can usually avoid being charged any interest. But if you carry a balance, interest is charged based on your APR.

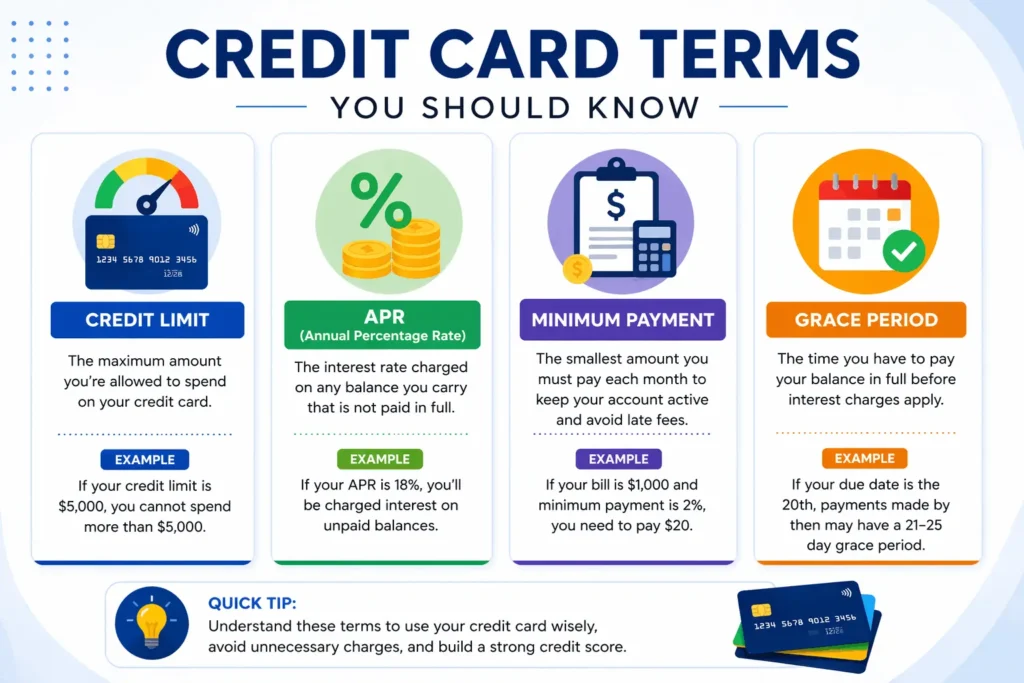

🔹 Important Terms Explained Clearly

Credit limit: the total amount you’re allowed to spend on your card

APR (Annual Percentage Rate): The interest rate on unpaid balances

Minimum payment: the smallest amount you’re required to pay on your balance each month

Grace Period: Time to pay without interest

Credit Utilization: Percentage of your limit used

👉 Example:

If your credit limit is $1,000 and you spend $300, your utilization is 30%. Keeping it below 30% helps your credit score.

Why Choosing the Right Credit Card Matters

Choosing the right credit card is one of the most important financial decisions you’ll make. Many people focus only on rewards but ignore fees, interest rates, and long-term value.

A good credit card can help you:

- Build or improve your credit score

- Earn cashback or travel rewards

- Save money through low interest or 0% APR offers

- Get protection on purchases

On the other hand, the wrong card can lead to:

- High-interest debt

- Unnecessary annual fees

- Poor credit management

👉 The best credit card is the one that fits your financial goals, not just the one with the biggest rewards.

Types of Credit Cards in the USA (Detailed Guide + Examples)

Now let’s take a closer look at the best credit card in the USA 2026 by breaking down each major type. We’ll explore how these top credit cards in the USA work, who they’re best suited for, and review real examples to help you choose the best credit card for your credit score and financial goals.

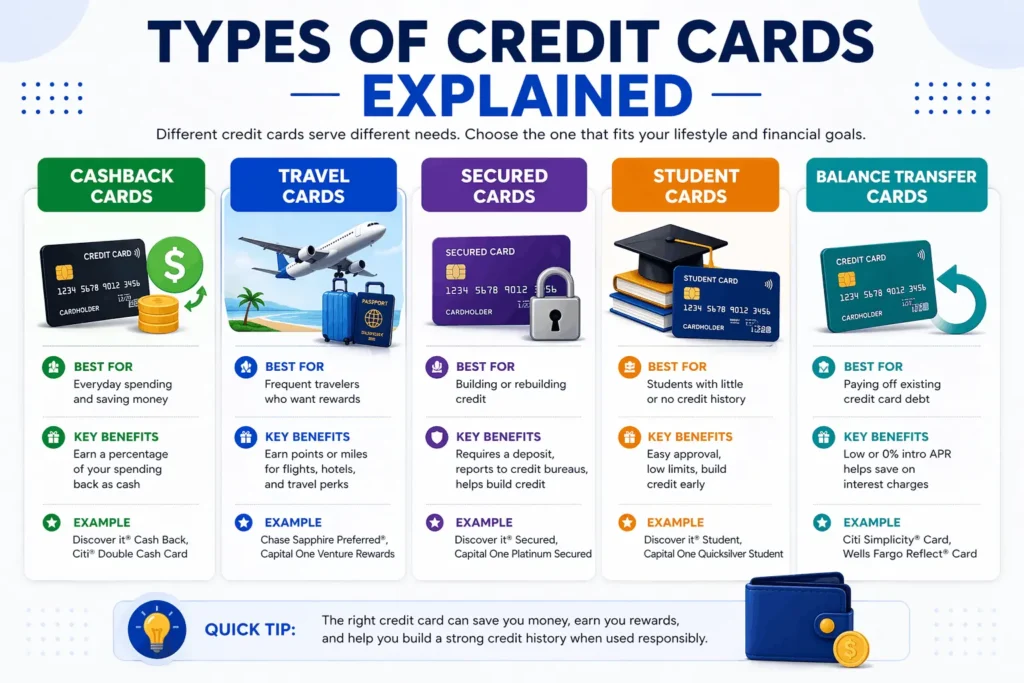

1. Cashback Credit Cards

Cashback credit cards give you a percentage of your spending back as cash rewards. This is one of the simplest and most popular reward systems in the U.S.

🔹 How Cashback Works

- You earn cashback based on your purchases:Flat rate (e.g., 2% on everything)

- Category-based (e.g., 3% dining, 5% groceries)

- Rotating categories (change every quarter)

🔹 Real Examples

✔️ Discover it® Cash Back

- 5% cashback on rotating categories

- Cashback match first year

👉 Example:

If you earn $500 in cashback over the year, Discover will match it—turning your total rewards into $1,000.

✔️ Citi® Double Cash Card

- 2% cashback total (1% when you buy + 1% when you pay)

✔️ Chase Freedom Unlimited®

- Flat cashback + bonus categories

🔹 Who Should Choose Cashback Cards?

- Everyday spenders

- Beginners

- People who want simple rewards

🔹 Pros and Cons

👍 Pros:

- Easy to understand

- Real cash value

- No complicated redemption

👎 Cons:

- Lower rewards than travel cards (sometimes)

- Category limits

2. Travel Credit Cards

Travel credit cards reward you with points or miles that can be used for travel-related expenses.

🔹 How Travel Rewards Work

You earn points when you spend, which can be redeemed for:

- Flights

- Hotels

- Car rentals

Some cards offer sign-up bonuses worth hundreds of dollars.

🔹 Real Examples

✔️ American Express Gold Card

- High rewards on dining and groceries

- Travel points

✔️ Chase Sapphire Preferred®

- Travel rewards + bonus points

- Flexible redemption

✔️ Capital One Venture Rewards Card

- Flat-rate miles on all purchases

🔹 Who Should Choose Travel Cards?

- Frequent travelers

- People who spend on dining and flights

🔹 Pros and Cons

👍 Pros:

- High-value rewards

- Travel perks

👎 Cons:

- Annual fees

- Complex redemption

3. Secured Credit Cards

Secured cards are designed for people with bad or no credit.

🔹 How Secured Cards Work

You deposit money as security, which becomes your credit limit.

👉 Example:

Deposit $200 → Credit limit $200

🔹 Real Examples

✔️ Capital One Platinum Secured

- Low deposit requirement

- Builds credit

✔️ Discover it® Secured Credit Card

- Cashback + credit building

🔹 Who Should Choose Secured Cards?

- Beginners

- People rebuilding credit

🔹 Pros and Cons

👍 Pros:

- Easy approval

- Improves credit score

👎 Cons:

- Requires deposit

- Lower limits

4. Student Credit Cards

Student credit cards are tailored for college students with little or no credit history.

🔹 Features

- Lower credit limits

- Easier approval

- Educational tools

🔹 Real Examples

✔️ Discover it® Student Cash Back

- Cashback rewards

- Good grades bonus

✔️ Capital One Quicksilver Student

- Flat cashback

🔹 Who Should Choose Student Cards?

- College students

- First-time users

5. Balance Transfer Credit Cards

These cards help you manage debt by offering 0% APR for a limited time.

🔹 How It Works

You transfer your existing debt to a new card with 0% interest.

👉 Example:

Transfer $3,000 → Pay it off in 12–18 months with no interest

🔹 Real Examples

✔️ Citi Simplicity® Card

- 0% APR intro period

- No late fees

✔️ Wells Fargo Reflect® Card

- Long intro APR period

🔹 Who Should Choose These Cards?

- People with existing credit card debt

🔹 Pros and Cons

👍 Pros:

- Save on interest

- Faster debt payoff

👎 Cons:

- Balance transfer fees

- Requires good credit

Credit Score and Best Card Strategy

Your credit score determines your options.

✔️ 750+ (Excellent): Premium cards

✔️ 700+ (Good): Cashback/rewards cards

✔️ 650+ (Fair): Limited options

✔️ Below 650: Secured cards

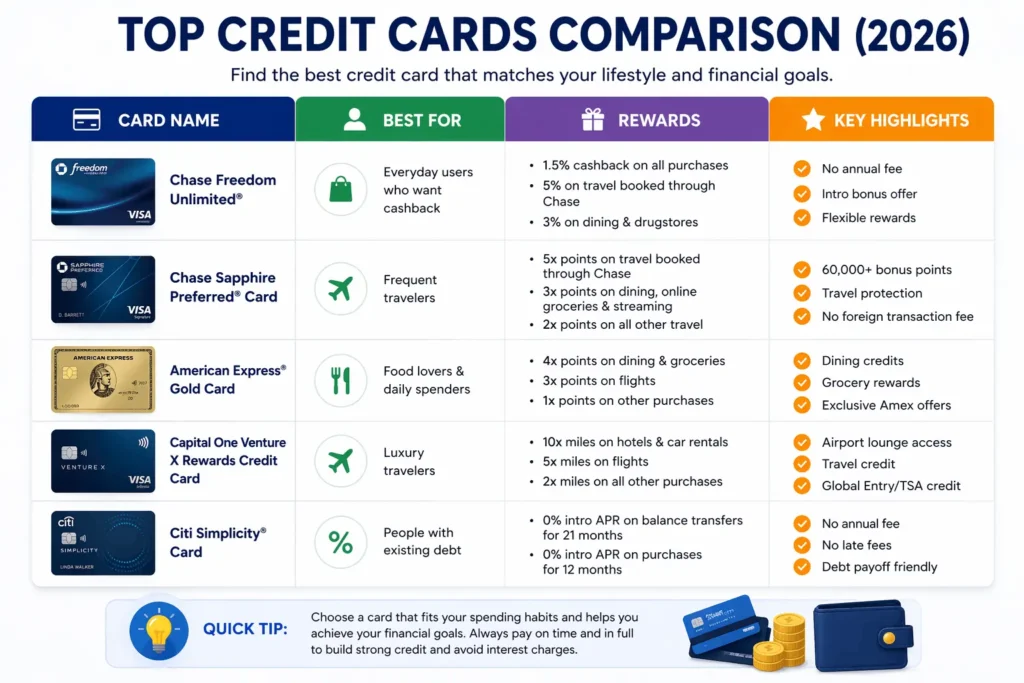

More Top Credit Card Examples in the USA (2026) – Detailed Breakdown

To make this guide more practical and useful, let’s take a closer look at some additional top credit cards in the USA (2026). These cards are widely used and trusted, but more importantly, each one serves a different type of user.

Rather than simply listing the features, we’ll take a deeper look by breaking them down clearly:

- How each card works

- Real-life use cases

- Pros and cons

- Who should apply

- Who should avoid

This will help you choose the right card based on your financial situation.

🟢 Blue Cash Preferred® Card from American Express

The Blue Cash Preferred® Card from American Express is one of the most powerful cashback cards in the U.S., especially for families and everyday spenders.

🔹 How This Card Works

This card focuses heavily on high cashback in everyday categories, particularly groceries and streaming services.

Typical reward structure includes:

- High cashback on U.S. supermarkets (up to a yearly limit)

- Cashback on streaming subscriptions

- Cashback on gas and transit

- Lower cashback on all other purchases

👉 Example:

If you spend $500 per month on groceries, you can earn significant cashback over the year, making this card extremely valuable for households.

✔️ Key Benefits

- One of the highest cashback rates for grocery spending

- Rewards on popular streaming platforms

- Strong value for families with regular expenses

👍 Pros

- Excellent cashback for everyday categories like groceries and gas

- Ideal for families and consistent spenders

- High long-term value if you maximize bonus categories

👎 Cons

- Annual fee (which may not be worth it for low spenders)

- Cashback categories have limits

- Less valuable for travel compared to points-based cards

👤 Who Should Apply?

- Families with high grocery spending

- People who spend regularly on streaming and gas

- Users who want predictable, high cashback

🚫 Who Should Avoid?

- Low spenders who won’t offset the annual fee

- People looking for travel rewards instead of cashback

- Those who prefer simple flat-rate cashback cards

🟢 Capital One Venture X Rewards Credit Card

The Capital One Venture X Rewards Credit Card is a premium travel card designed for users who want luxury benefits and high-value rewards.

🔹 How This Card Works

This card offers miles instead of cashback, which can be redeemed for travel purchases such as flights and hotels.

You earn:

- Flat-rate miles on all purchases

- Higher rewards on travel bookings

- Large welcome bonus (if eligible)

👉 Example:

If you spend $2,000 per month, you can accumulate a large number of miles that can be used for free flights or hotel stays.

✔️ Key Benefits

Enjoy high-end travel benefits like complimentary airport lounge access and valuable travel credits that help reduce your trip expenses.

- High rewards rate on all purchases

- Strong welcome bonus

👍 Pros

- Excellent for frequent travelers

- Simple flat-rate miles earning system

- Valuable travel credits that offset annual fee

👎 Cons

- High annual fee

- Requires good to excellent credit

- Rewards are best used for travel, not cashback

👤 Who Should Apply?

- Frequent travelers (domestic or international)

- People who can use travel perks like lounge access

- Users who spend consistently and want premium benefits

🚫 Who Should Avoid?

- Beginners or users with low credit scores

- People who rarely travel

- Ideal for those who prefer to avoid paying an annual fee

🟢 Bank of America® Customized Cash Rewards Credit Card

The Bank of America® Customized Cash Rewards Credit Card is a flexible cashback card that allows you to choose your bonus category.

🔹 How This Card Works

This card is unique because it lets you select your 3% cashback category, such as:

- Online shopping

- Dining

- Gas

- Travel

👉 Example:

If you shop online frequently, you can set your category to “online shopping” and earn higher cashback on those purchases.

✔️ Key Benefits

- Flexible rewards system

- No annual fee

- Ability to adjust categories based on spending

👍 Pros

- Customizable cashback categories

- Good for targeted spending

- No annual fee makes it beginner-friendly

👎 Cons

- Cashback limits on bonus categories

- Requires tracking your selected category

- Not ideal for people who want a fully automatic system

👤 Who Should Apply?

- People with specific spending habits (like online shopping or gas)

- Users who want control over their rewards

- Beginners who want a no-fee cashback card

🚫 Who Should Avoid?

- People who don’t want to manage categories

- Users looking for premium rewards or travel perks

- High spenders who may hit category limits

🟢 Discover it® Secured Credit Card

The Discover it® Secured Credit Card is one of the best options for building or rebuilding credit while still earning rewards.

🔹 How This Card Works

Unlike most secured cards, this one offers cashback rewards, which makes it stand out.

You place a refundable security deposit upfront, and that amount is used as your credit limit. At the same time, you earn cashback on purchases.

👉 Example:

Deposit $300 → Credit limit $300 → Earn cashback while building credit

✔️ Key Benefits

- Cashback rewards on a secured card

- Reports to all major credit bureaus

- Opportunity to upgrade to an unsecured card

👍 Pros

- Combines credit building with rewards

- High approval chances

- No annual fee

👎 Cons

- Requires upfront deposit

- Lower credit limit compared to unsecured cards

- Not suitable for long-term premium use

👤 Who Should Apply?

- Beginners with no credit history

- People rebuilding poor credit

- Users who want rewards while building credit

🚫 Who Should Avoid?

- People with good or excellent credit

- Users looking for high credit limits

- Those who don’t want to deposit money upfront

Final Thoughts on These Credit Card Options

Each of these credit cards serves a different purpose, and there is no single “best” option for everyone.

- If you’re aiming to get the most cashback from your everyday purchases, the Blue Cash Preferred® Card is a great option to consider.

- If you’re looking for top-tier travel rewards and perks, the Capital One Venture X is a standout choice.

- If you want flexible rewards without worrying about an annual fee, the Bank of America® Customized Cash Rewards card is a great option.

- If you need to build or rebuild credit, Discover it® Secured is one of the best starting points.

👉 The smartest approach is to choose a card based on:

- Your spending habits

- Your long-term financial goals

How to Choose the Best Credit Card (Advanced Strategy)

Choosing a credit card is not just about rewards—it’s about long-term value.

Start by checking your credit score and financial goals. Then compare multiple cards based on:

- APR

- Fees

- Rewards structure

- Intro offers

Always think long-term. A card that saves you money over time is better than one that offers short-term rewards.

How to Apply for a Credit Card (Step-by-Step)

- Choose the right card

- Fill out application

- Submit documents

- Wait for approval

Smart Tips to Use Credit Cards Like a Pro

- Pay full balance every month

- Keep utilization below 30%

- Use auto-pay

- Track spending

- Avoid unnecessary debt

Common Mistakes to Avoid

- Applying for too many cards

- Missing payments

- Ignoring fees

- Carrying high balances

- Choosing wrong card type

Conclusion

In conclusion, choosing the best credit card in the USA 2026 starts with understanding your personal financial needs, spending habits, and long-term goals. There’s no one-size-fits-all option, as even the top credit cards in the USA are designed for different types of users and purposes.

If you’re just starting out, focus on finding the best credit card for beginners to build and improve your credit through responsible use. Those with a solid credit history can maximize value by selecting from the best rewards credit cards, taking advantage of cashback, travel perks, and premium benefits. On the other hand, if you’re dealing with existing debt, choosing a low-interest or balance transfer option can help reduce financial pressure.

👉 Ready to choose your first credit card? Compare top options and apply with confidence today.

FAQs About the Best Credit Cards in the USA (2026)

What is the best credit card in the USA for beginners?

The best credit card in the USA for beginners typically includes secured credit cards or entry-level cashback cards like Discover it®. These options help build credit while offering simple rewards on everyday spending.

What credit score is needed for a credit card?

Most credit cards in the USA require a credit score of 650 or higher for approval. However, secured credit cards and beginner options are available for individuals with lower or limited credit history.

Which credit card gives the most cashback?

The best cashback credit cards in the USA often feature rotating bonus categories or high flat-rate rewards. Choosing the right card depends on your spending habits and preferred reward structure.

Are travel credit cards worth it?

Travel credit cards in the USA are worth it if you travel frequently and take full advantage of rewards, lounge access, and travel credits. They provide significant value when used strategically.

Can I get a credit card with no income?

Getting a credit card in the USA without income can be challenging, but students or applicants with alternative income sources may still qualify. Secured cards are also a practical option.

How many credit cards should I have?

For most users in the USA, having 2–4 credit cards is considered ideal. This allows you to diversify rewards while maintaining a manageable credit utilization ratio.

Does applying hurt credit score?

Applying for a credit card in the USA may temporarily lower your credit score due to a hard inquiry. However, the impact is usually small and recovers over time with responsible use.

What is a 0% APR credit card?

A 0% APR credit card in the USA offers an introductory period with no interest on purchases or balance transfers. This feature is useful for managing large expenses or consolidating debt.

How do I build credit fast?

To build credit quickly in the USA, make on-time payments, keep your credit utilization low, and use your credit card regularly. Consistent habits are key to improving your credit score.

Should I cancel old credit cards?

It is generally not recommended to cancel old credit cards in the USA, as they contribute to your credit history length. Keeping them open can positively impact your overall credit score.