How to increase your credit score by 100 points is one of the most common questions Americans ask when they want better loan approvals, lower interest rates, or access to premium credit cards.

A higher credit score can make a huge difference in your financial life. It may help you qualify for lower mortgage rates, reduce the cost of car loans, and improve your chances of getting approved for new credit.

The good news is that many people can increase their credit score by 100 points by making a few smart financial changes and sticking to them consistently. While there is no overnight solution, understanding how credit scores work and focusing on the factors that matter most can produce significant results over time.

In this guide, you’ll learn practical strategies used by many Americans to build stronger credit and improve their financial future.

Official U.S. government consumer credit information

Table of Contents

How Can You Increase Your Credit Score by 100 Points?

How to increase your credit score by 100 points often comes down to improving the key factors that influence your credit report. Paying bills on time, lowering credit card balances, fixing report errors, and avoiding unnecessary credit applications can all help raise your score.

Pay Bills on Time

Paying bills on time is one of the fastest ways to build a positive credit history. Payment history is the largest factor used in most credit scoring models.

For example, if Sarah from Texas has a credit card payment due on the 15th of each month, setting up automatic payments can help her avoid late fees and protect her credit score.

Even one missed payment can remain on a credit report for years, so consistency matters.

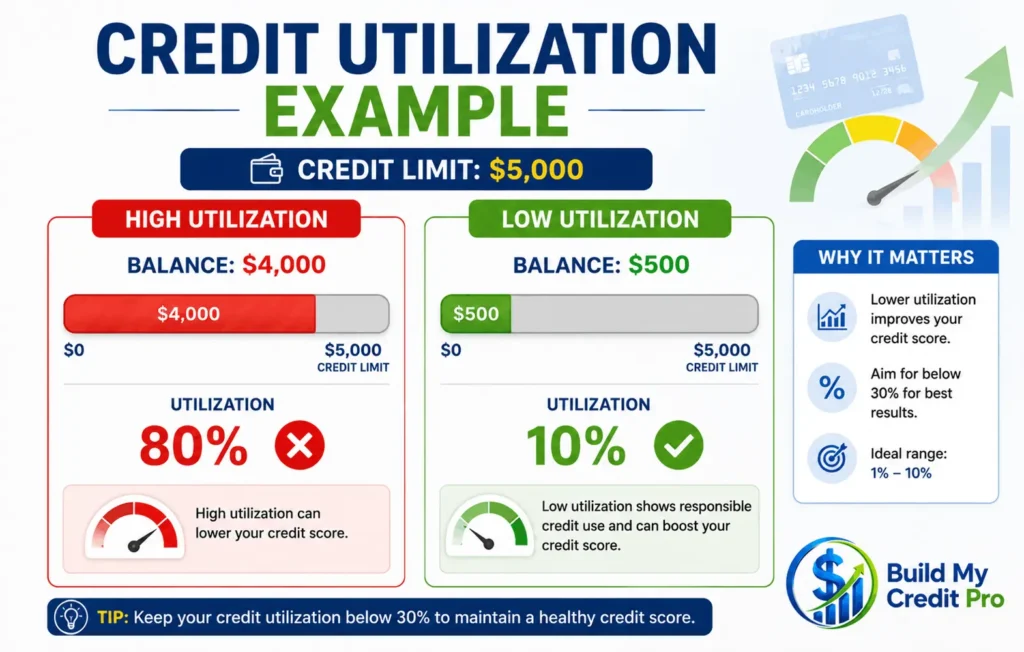

Lower Credit Utilization

Lowering credit utilization can quickly improve your credit score if you’re carrying high credit card balances.

Let’s say your total credit limit is $10,000 and your current balance is $4,000. Your credit utilization ratio is 40%.

Reducing your balance to $1,000 lowers your credit utilization rate to 10%, a level that is typically considered positive by most credit scoring systems.

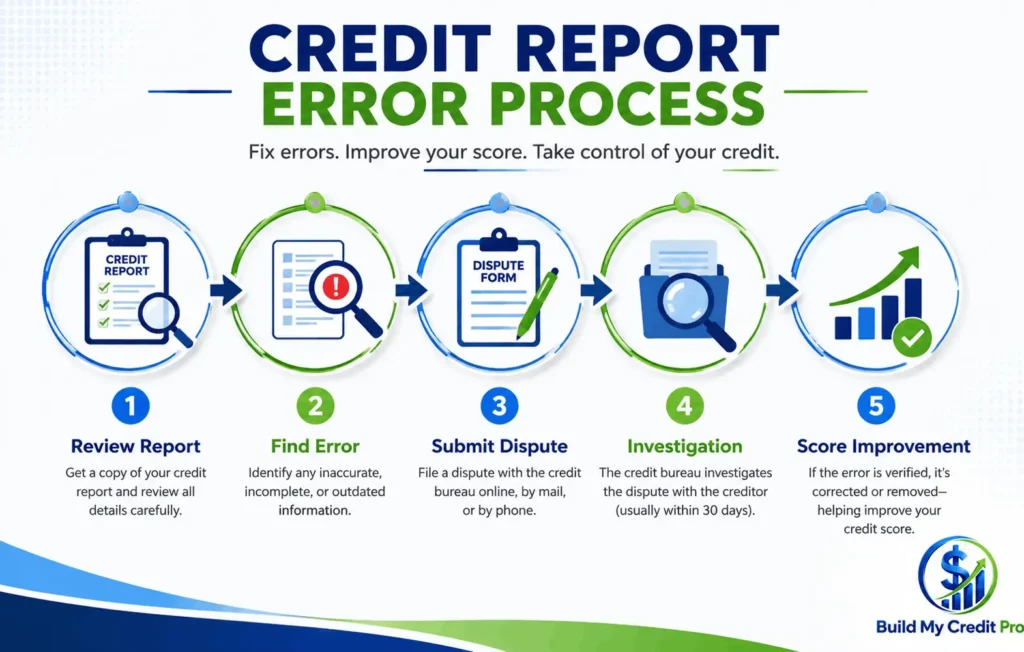

Fix Credit Report Errors

Fixing credit report errors can remove inaccurate information that may be lowering your score unfairly.

For example, John from Florida discovered a credit card account on his report that did not belong to him. After filing a dispute and having the account removed, his credit score improved within a few months.

Always review your credit reports carefully for mistakes.

Avoid New Hard Inquiries

Avoiding new hard inquiries can help protect your score while you’re working to rebuild credit.

Applying for several credit cards within a short period may signal financial stress to lenders. Avoid seeking new credit unnecessarily, and submit applications only when they are truly needed.

Understanding Credit Scores in the USA

What Is a Credit Score?

A credit score is a three-digit number that helps lenders determine how likely you are to repay borrowed money.

American credit scores generally fall within a scoring range of 300 at the low end and 850 at the high end. The higher your score, the less risky you appear to lenders.

A credit score can play an important role when seeking approval for:

- Auto loans

- Mortgages

- Apartment rentals

Credit Score Ranges Explained

Credit score ranges help lenders evaluate your creditworthiness.

Typical ranges include:

- Poor: 300–579

- Fair: 580–669

- Good: 670–739

- Very Good: 740–799

- Excellent: 800–850

For example, someone with a 760 credit score may qualify for better loan terms than someone with a 620 score.

Why Lenders Care About Your Credit Score

Your credit score helps lenders assess risk. A higher score often leads to better borrowing opportunities and lower interest rates.

For example, two borrowers may apply for the same car loan. The applicant with a higher credit score could receive a lower interest rate and save hundreds or even thousands of dollars over the life of the loan.

Can a Credit Score Improve by 100 Points in a Short Time?

Increasing your credit score by 100 points is possible for many consumers, especially if their score has been affected by high credit card balances, missed payments, or reporting errors.

However, results vary depending on your individual credit profile.

Factors That Determine Your Results

Your credit score improvement timeline is affected by several key factors.

These include:

- Payment history

- Age of credit accounts

- Total debt

- Credit mix

- Recent credit inquiries

Someone starting with a score of 580 may see larger gains than someone who already has a score above 700.

How Fast Credit Scores Can Improve

Many people are surprised by how quickly their credit score can improve, but consistent effort and patience remain essential.

For example, if you pay off a large credit card balance, the updated information may be reported within one or two billing cycles. This could result in a noticeable score increase within a few weeks.

Other improvements, such as building a long history of on-time payments, may take several months to show their full impact.

The most successful credit-building strategy is consistency. Small positive actions repeated every month can lead to substantial score increases over time.

10 Proven Ways to Increase Your Credit Score by 100 Points

Pay Every Bill on Time

Paying every bill on time is one of the most effective ways to increase your credit score by 100 points. Your payment history makes up a large portion of your credit score, so even one late payment can have a negative impact.

For example, if you consistently pay your credit card, auto loan, and utility bills before the due date, lenders see you as a responsible borrower. By setting up autopay, you can make timely payments more consistent and avoid accidental late payments.

Reduce Your Credit Utilization Below 30%

Reducing your credit utilization below 30% can improve your credit score relatively quickly.

Credit utilization measures how much of your total available credit limit is currently being used. If your total credit limit is $5,000 and your balance is $2,000, your utilization rate is 40%.

Paying your balance down to $1,500 or less would bring your utilization below 30%, which is generally considered healthier for your credit score.

Aim for a Utilization Rate Below 10%

Aiming for a utilization rate below 10% can provide even greater credit score benefits.

Many consumers with excellent credit scores keep their utilization in the single digits.

For example, if your credit card limit is $10,000, keeping your balance below $1,000 may help maximize your score potential.

Check Your Credit Reports for Errors

Carefully checking your credit reports can reveal errors that could be dragging down your credit rating.

Look for:

- Incorrect account balances

- Credit accounts that are not associated with your name

- Duplicate accounts

- Incorrect payment histories

Reviewing your reports regularly allows you to catch mistakes before they cause long-term damage.

Dispute Inaccurate Information

Disputing inaccurate information can lead to credit score improvements if errors are removed.

For example, if a credit report incorrectly shows a missed payment that was actually paid on time, correcting that error could help improve your score.

Always keep documentation that supports your dispute.

Become an Authorized User

Joining a well-managed credit card account as an authorized user can be an effective way to establish or improve credit history.

A credit card account with a long history of on-time payments and low utilization can potentially add favorable information to your credit profile when you are an authorized user.

For example, a young adult may become an authorized user on a parent’s credit card to start building credit.

Keep Older Credit Accounts Open

Older accounts often add value to your credit history length, so keeping them active may be beneficial.

A longer account history can positively influence your credit score because account age is an important scoring factor.

Even if you no longer use an older credit card frequently, keeping it open may benefit your score if there are no annual fees.

Avoid Applying for Multiple New Accounts

Avoiding multiple credit applications can protect your score from unnecessary hard inquiries.

As an example, applying for multiple credit cards in the same month can make lenders more cautious about extending credit.

Only apply for new credit when it serves a specific purpose.

Pay Down Revolving Debt

Paying down revolving debt can lower your credit utilization and improve your financial health.

Credit card debt that is carried from one month to the next is commonly classified as revolving debt.

Paying more than the minimum payment each month helps reduce debt faster and may lead to credit score improvements.

Use a Secured Credit Card Responsibly

Using a secured credit card responsibly can help people with limited or damaged credit rebuild their scores.

A secured card requires a refundable security deposit that usually becomes your credit limit.

For example, someone rebuilding credit may open a secured card with a $300 deposit and make small purchases while paying the balance in full each month.

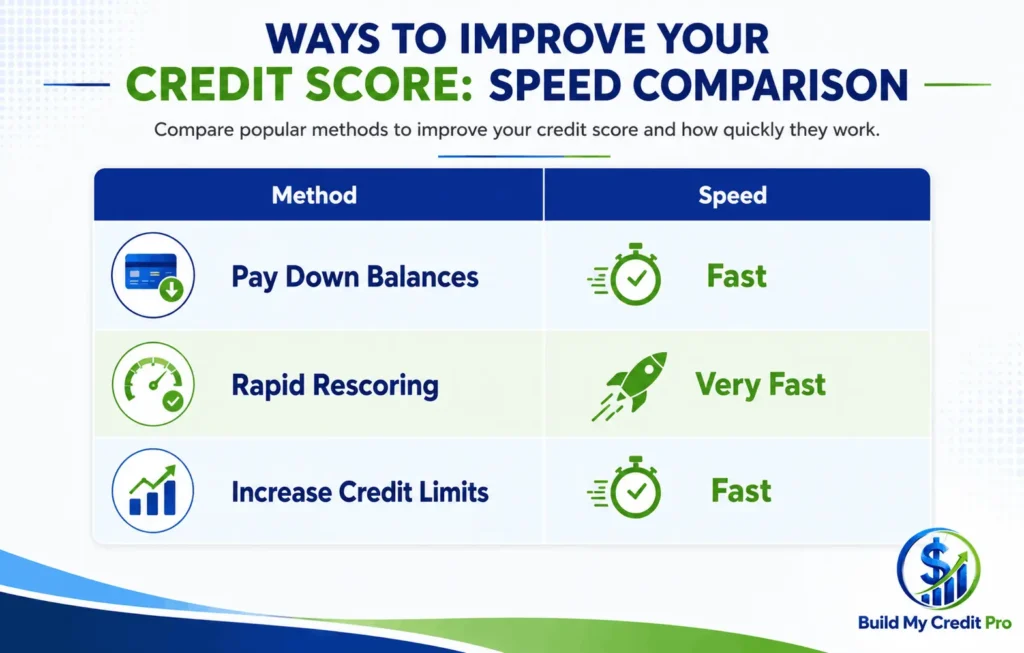

Quick Strategies to Improve Your Credit Score

Rapid Rescoring

Rapid rescoring is a process sometimes used by mortgage lenders to update credit information quickly after errors are corrected or balances are paid down.

This option is not available to everyone, but it may help borrowers seeking a mortgage approval.

Paying Down Credit Card Balances

Paying down credit card balances is often one of the fastest ways to increase your credit score by 100 points.

A reduction in reported balances may lower your utilization rate, which can have a positive effect on your credit score once the updated information reaches the credit bureaus.

Increasing Available Credit

Increasing available credit can reduce your utilization ratio if spending remains the same.

For example, if your credit limit increases from $5,000 to $10,000 while your balance stays at $1,000, your utilization falls from 20% to 10%.

Common Credit Score Mistakes to Avoid

Closing Old Accounts

Closing old accounts can shorten your average account age and reduce available credit.

Before closing an account, consider how it may affect your credit score.

Missing Payment Due Dates

Failing to make payments by their due dates can have a serious negative impact on your credit score.

Even a single late payment can remain on your credit report for years and may affect future loan approvals.

Maxing Out Credit Cards

Maxing out credit cards increases your utilization ratio and may signal financial stress to lenders.

Using nearly all of your available credit—such as $4,900 of a $5,000 limit—can produce a high utilization ratio and put downward pressure on your credit score.

Applying for Too Much Credit

Applying for too much credit within a short period can lead to multiple hard inquiries.

This may temporarily lower your score and raise concerns among potential lenders.

Can You Raise Your Credit Score by 100 Points Quickly?

Within 30 Days

Increasing your credit score within 30 days is possible in some situations.

Paying down high credit card balances or correcting reporting errors may produce noticeable improvements within one reporting cycle.

Within 3–6 Months

Increasing your credit score within 3 to 6 months is a realistic goal for many Americans.

Consistently paying bills on time, reducing debt, and maintaining low utilization can create meaningful progress during this period.

For example, an individual with a 620 credit score may be able to move into the good credit range over time by maintaining strong financial habits and using credit responsibly.

Within 12 Months

Increasing your credit score within 12 months is achievable for many consumers who stay committed to improving their credit.

Individuals recovering from missed payments, high debt levels, or past credit problems often see substantial improvements over a year of responsible credit management.

The key is consistency. Small actions repeated month after month often lead to the biggest long-term credit score gains.

Free Tools to Track Your Credit Score Progress

Credit Monitoring Services

Credit monitoring services can help you track changes in your credit score and receive alerts when important updates appear on your credit report.

Many banks and credit card companies now offer free credit score monitoring as a customer benefit. These services can notify you about new accounts, hard inquiries, or significant changes to your credit profile.

For example, if your credit score increases after paying down a large credit card balance, a credit monitoring service may alert you as soon as the update is reported.

Regular monitoring helps you stay informed and identify potential issues before they become serious problems.

Credit Report Websites

Credit report websites allow you to review the information that lenders see when evaluating your creditworthiness.

Checking your credit reports regularly is one of the smartest steps you can take when learning how to increase your credit score by 100 points.

When reviewing your reports, pay attention to:

- Account balances

- Payment history

- Personal information

- Open and closed accounts

- Credit inquiries

For example, if you notice an account that doesn’t belong to you, reporting the error quickly may help prevent unnecessary damage to your credit score.

Mobile Credit Tracking Apps

Mobile credit tracking apps make it easy to monitor your credit score directly from your smartphone.

Many apps provide:

- Credit utilization tracking

- Personalized credit tips

- Alerts about major credit changes

For example, if your utilization rate rises above 30%, a credit tracking app may notify you so you can take action before it affects your score.

These tools can help you stay motivated and measure your progress over time.

FAQ: How to Increase Your Credit Score by 100 Points

Can I increase my credit score by 100 points in 30 days?

While a 100-point credit score increase in 30 days is possible for some people, it usually depends on factors such as high credit card balances, reporting errors, or recent negative marks. Most consumers see the best results over several months of responsible credit use.

What is the fastest way to increase your credit score by 100 points?

The fastest way to increase your credit score is to pay down credit card balances, make every payment on time, dispute inaccurate information, and keep your credit utilization below 30%. These actions can lead to noticeable improvements in a relatively short period.

How much can paying off credit cards improve my credit score?

Paying off credit card debt can significantly improve your credit score because it lowers your credit utilization ratio. A lower credit utilization ratio often leads to a stronger credit profile. Many Americans notice positive credit score improvements after keeping their credit card balances below 30% of their total available credit limit.

Can removing late payments help increase your credit score?

Yes. If a late payment is reported incorrectly, disputing and removing it may help increase your credit score. Accurate late payments can remain on your credit report for up to seven years, but some lenders may grant a goodwill adjustment.

How long does it take to increase your credit score by 100 points?

The timeline varies based on your credit history and current score. Some people may increase their credit score by 100 points within three to six months, while others may need a year of consistent credit-building habits.

What credit utilization ratio is best for improving a credit score?

For the best results, keep your credit utilization below 10%. Lower utilization signals responsible credit management and can help improve your credit score faster than carrying high balances.

Will opening a new credit card increase my credit score?

Opening a new credit card can help increase your credit score if it lowers your overall credit utilization and you make payments on time. However, applying for multiple cards at once may temporarily lower your score.

What mistakes should I avoid when trying to increase my credit score?

Avoid missing payments, maxing out credit cards, closing old accounts, and applying for too much new credit. These common mistakes can slow down your efforts to increase your credit score and maintain good credit health.

Final Thoughts

How to increase your credit score by 100 points is not about finding a quick fix. It’s about developing smart financial habits and consistently making decisions that strengthen your credit profile.

Simple actions such as paying bills on time, reducing credit utilization, reviewing credit reports for errors, and avoiding unnecessary debt can make a significant difference over time.

For example, someone with a credit score of 580 who consistently pays bills on time, lowers credit card balances, and corrects report errors may be able to move into the good credit range within several months.

The key is patience and consistency. Every positive action you take today can help build a stronger credit score tomorrow.

By following the strategies in this guide, you’ll be in a better position to increase your credit score, qualify for better financial products, and achieve your long-term financial goals in the United States.