If you’re starting your credit journey in the United States, one of the most important concepts you need to understand is the credit usage ratio. It may sound technical at first, but in reality, it’s one of the easiest parts of your credit score to control.

Many beginners focus only on paying bills on time. While that’s essential, your utilization credit card usage can quickly raise or lower your score—even if you never miss a payment.

In fact, people with excellent credit scores don’t just pay on time—they also keep their utilization credit low at all times.

Credit usage ratio is the percentage of available credit you are currently using. In the USA, experts recommend keeping your utilization below 30% to maintain a healthy credit score.

Table of Contents

What is Credit Utilization Ratio?

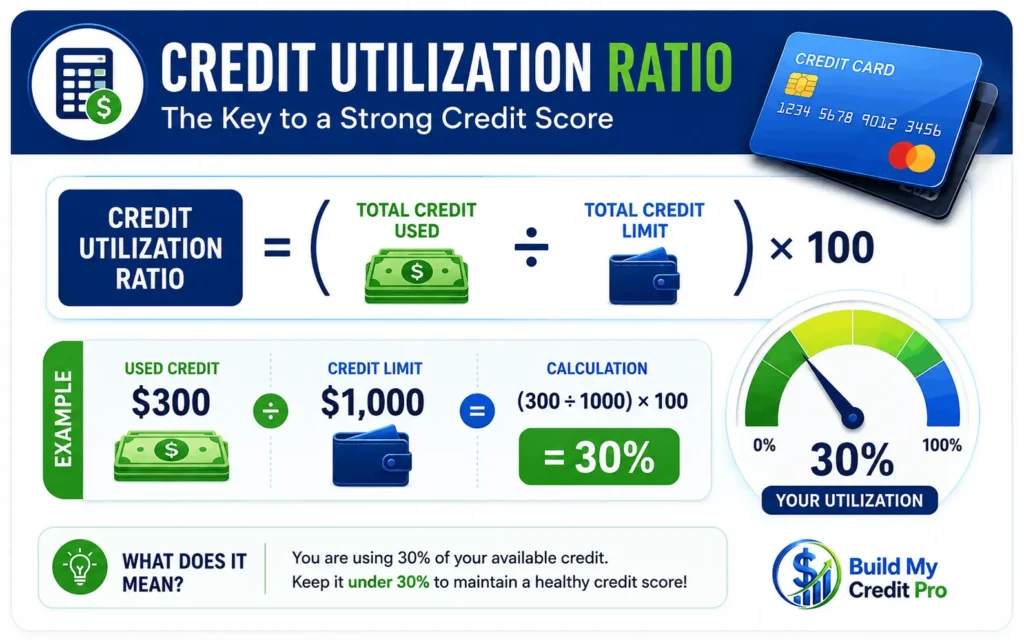

credit balance ratio is the percentage of your total available credit that you are currently using. It’s determined by taking your total credit card balances, dividing them by your overall credit limit, and then converting that number into a percentage. Keeping your utilization credit low helps improve your credit score.

Simple Beginner Definition

Your credit utilization ratio is the percentage of your total available credit that you’re currently using.

Formula Explained Clearly

- Credit Utilization Ratio = (Total Credit Used ÷ Total Credit Limit) × 100

This formula is used by lenders and credit scoring models to measure your utilization credit behavior.

Real-Life Example of Utilization Credit Card Usage

Let’s say you have one credit card:

- Credit limit: $1,000

- Current balance: $300

👉 Your credit utilization ratio is:

- (300 ÷ 1000) × 100 = 30%

This is considered acceptable, but not ideal if you want a high score.

Another Example (Multiple Cards)

Now let’s look at a more realistic U.S. scenario:

- Card 1 limit: $2,000 → used $500

- Card 2 limit: $3,000 → used $1,000

👉 Total credit limit = $5,000

👉 Total used = $1,500

- (1500 ÷ 5000) × 100 = 30%

Even though your overall credit balance ratio is 30%, one card may still have higher usage, which can impact your score.

Why Utilization Credit is So Important in the USA

In the U.S., most lenders rely on your FICO Score when evaluating your creditworthiness.

How Much It Affects Your Score

- Credit utilization ratio = about 30% of your credit score

- It’s considered the second most influential factor, right after your payment history

How Lenders Interpret Your Utilization Credit

Think of it this way:

- Low utilization credit → You’re in control of your finances

- High utilization credit → You might be relying too much on borrowed money

Even if you pay your bill in full every month, high utilization credit card balances can still signal risk.

What is a Good Credit Utilization Ratio?

A good credit usage ratio is below 30%, but for the best results, it should be under 10%. Lower utilization credit shows lenders that you manage credit responsibly and can help increase your credit score faster.

Ideal Ranges Explained

- ✅ 1% – 10% (Excellent): Best for high scores like 750–800

- 👍 10% – 30% (Good): Safe range for most users

- ⚠️ Above 30% (Risky): Can start lowering your score

- ❌ Above 75% (Very Risky): Major negative impact

👉 If your goal is to build excellent credit, aim to keep your credit usage ratio under 10%.

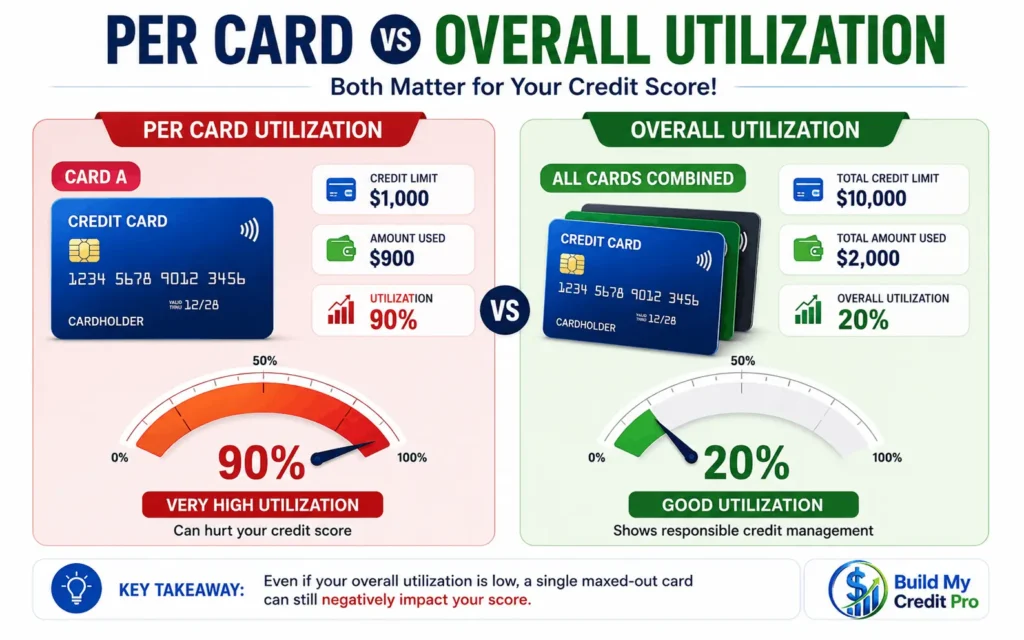

Per Card vs Overall Utilization Credit Card Usage

Per Card Utilization

Each card has its own utilization credit ratio.

👉 Example:

- Limit: $1,000

- Used: $900 → 90% utilization (very high)

Overall Utilization

This includes all your cards combined.

👉 Example:

- Total limit: $10,000

- Total used: $2,000 → 20% utilization (good)

Why Both Matter

Many beginners think only overall utilization matters—but that’s not true.

👉 A single maxed-out card can hurt your score, even if your total utilization credit looks fine.

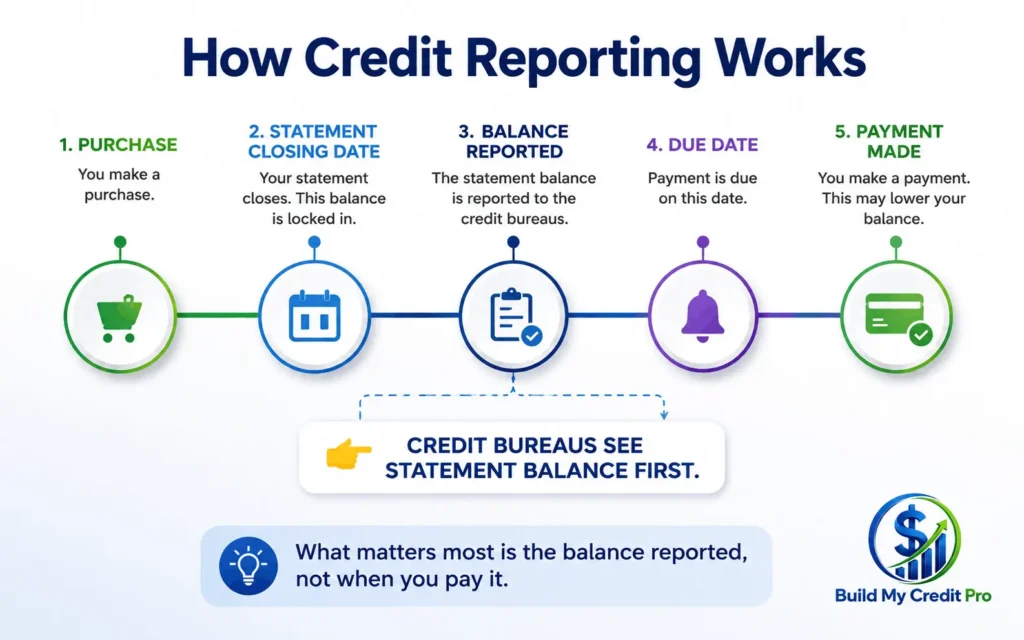

When Credit Utilization is Reported (Critical for Beginners)

Credit usage is usually reported on your statement closing date, not your payment due date. This means your utilization credit card balance at that time is what affects your credit score.

Statement Date vs Due Date

- Statement Date: When your balance is reported to credit bureaus

- Due Date: When payment is due

👉 Important: Your credit usage ratio is based on what gets reported—not what you pay later.

Real-Life Timing Example

- You spend $900 on a $1,000 card

- Statement closes → 90% utilization reported

- You pay full amount later

👉 Your score may still drop because of high utilization credit reported earlier.

Smart Strategies to Lower Your Utilization Credit Card Ratio

Pay Before the Statement Date

This is one of the most powerful tricks to control your credit usage ratio.

Make Multiple Payments Per Month

Paying weekly or bi-weekly helps keep your utilization credit low.

Request a Credit Limit Increase

Higher limits reduce your utilization credit card percentage instantly.

Use Multiple Cards Strategically

Spread expenses to maintain balanced utilization credit usage.

Keep Old Cards Open

Old accounts increase your total credit limit, lowering your credit usage ratio.

Common Mistakes Beginners Should Avoid

Maxing Out Cards

Using your full limit increases your utilization credit and lowers your score.

Closing Credit Cards

This lowers the amount of credit you have available and pushes your used credit percentage ratio higher.

Ignoring Reporting Dates

Your utilization credit card balance at reporting time matters the most.

Thinking Full Payment Fixes Everything

Even if you pay in full, high utilization at reporting can still hurt your score.

How Fast Can Credit Utilization Improve Your Score?

To improve utilization credit card usage fast, pay down your balances early, keep your usage below 30%, and increase your credit limit. These steps can quickly lower your used credit percentage ratio and boost your score.

Fast Results Explained

- Updates monthly

- Score can improve within 30 days

- Paying down balances gives immediate benefits

Tools to Monitor Utilization Credit in the USA

Tracking your credit usage ratio is easy with tools like:

These tools help you monitor and improve your utilization credit habits.

Advanced Strategy: The 1–5% Rule

Many credit experts recommend using only a very small portion of your credit.

Why This Works

- Shows active usage

- Keeps utilization extremely low

How Utilization Credit Helps You Reach an 800 Score

If your goal is a top-tier credit score:

- Keep credit usage ratio under 10%

- Combine with on-time payments

- Avoid unnecessary debt

This is one of the fastest ways to improve your credit profile in the U.S.

Frequently Asked Questions (FAQs) About Credit Utilization in the USA

What is credit utilization ratio and why is it important in the USA?

Credit utilization is the percentage of your available credit that you’re using on your credit cards. It’s important because it makes up a big part of your credit score, and high utilization can lower your score quickly.

What is a good credit utilization ratio in the USA?

A good credit utilization ratio is below 30%, but for the best credit score, experts recommend keeping it under 10%. Lower credit card utilization shows lenders you manage credit responsibly.

How does credit utilization affect your credit score?

Credit utilization directly impacts your credit score by showing how much of your credit limit you’re using. High utilization credit card balances can signal risk and reduce your score.

How can I lower my credit utilization quickly?

You can lower your credit utilization by paying down your credit card balances, making multiple payments each month, or requesting a credit limit increase. This reduces your utilization credit card ratio fast.

Does paying off a credit card improve credit utilization?

Yes, paying off your credit card lowers your credit utilization ratio immediately. This can help boost your credit score, especially if your utilization credit card usage was high before.

Is 0% credit utilization good for your credit score?

While 0% credit utilization sounds ideal, it’s not always the best. Using a small amount (like 1–10%) of your credit card and paying it off shows active and responsible credit use.

Do all credit cards affect your credit utilization?

Yes, all your credit cards are combined to calculate your overall credit utilization ratio. Both individual card utilization and total utilization credit card usage matter for your credit score.

How often is credit utilization reported to credit bureaus?

Most credit card issuers report your credit utilization to bureaus once a month, usually at the end of your billing cycle. That’s why timing your payments can help control your utilization credit card ratio.

Final Thoughts

Your credit usage ratio is one of the most powerful tools you have as a beginner.

It’s not about avoiding credit—it’s about using it wisely.

By controlling your utilization credit card usage, you can:

- Improve your score quickly

- Build strong financial habits

- Move closer to excellent credit