Introduction

Late payments can damage your financial future more than many people realize. A single missed payment can lower your credit score, reduce your chances of loan approval, and even affect credit cards, apartment rentals, or low interest rates. If you are trying to improve your financial health, learning how to remove late payments from your credit report is very important.

Many Americans struggle with missed payments because of job loss, emergencies, medical bills, or unexpected expenses. The good news is that some negative marks can be corrected or removed legally. If the information is inaccurate, outdated, or unfairly reported, you may be able to dispute it and improve your credit profile.

This complete 2026 guide explains how to remove late payments from your credit report, how credit bureaus report late payments, and the best ways to fix your credit score in the USA using simple and practical steps.

Table of Contents

What Is a Late Payment on a Credit Report?

A late payment appears on your credit report when you fail to make at least the minimum payment on a credit account before the due date. Credit card companies, lenders, and loan providers may report these missed payments to the major credit bureaus, which can negatively affect your credit score.

Payment history is one of the biggest factors used in credit scoring models. That is why understanding how to remove late payments from your credit report can help you rebuild credit and improve your financial opportunities.

How Credit Bureaus Report Late Payments

The three major credit bureaus in the USA are:

- Experian

- Equifax

- TransUnion

These credit bureaus receive account information from lenders every month. If your payment is overdue, the lender may report it as:

- 30 days late

- 60 days late

- 90 days late

- 120+ days late

The more late payments you have, the more your credit score may drop. Serious late payments can make lenders believe you are a high-risk borrower.

When a Payment Is Considered Late

Most lenders will charge a late fee immediately after the due date passes. However, a payment is usually not reported to the credit bureaus until it becomes at least 30 days overdue.

For example:

- Payment due date: June 1

- Payment made: June 12

Result: You may pay a late fee, but it may not appear on your credit report

Once the account becomes 30 days late, the lender can officially report the missed payment to the credit bureaus.

If you accidentally miss a payment, reach out to your lender as soon as possible to discuss your options and avoid further damage to your credit. In some cases, lenders may waive the late fee or avoid reporting the late payment if you have a strong payment history.

How Long Do Late Payments Remain on Your Credit Report in the USA?

In most cases, late payments remain on your credit report for up to 7 years from the original delinquency date.

Even after you pay the account, the late payment history may still appear on your report. However, the negative impact usually becomes smaller over time if you continue making on-time payments.

| Late Payment Type | Time on Credit Report |

|---|---|

| 30-day late payment | Up to 7 years |

| 60-day late payment | Up to 7 years |

| 90-day late payment | Up to 7 years |

| Collections or charge-offs | Up to 7 years |

If the late payment information is incorrect, duplicated, or unverifiable, you may have the legal right to dispute it. Understanding how to remove late payments from your credit report can help improve your credit score and increase your chances of getting approved for loans and credit cards in the future.

How Late Payments Affect Your Credit Score

Late payments can have a major impact on your financial life. Your payment history is one of the most important parts of your credit score, which means even one missed payment can hurt your credit profile. If you are trying to improve your score or learn how to remove late payments from your credit report, it is important to understand how these negative marks affect lenders and credit bureaus.

A lower credit score can make it harder to qualify for personal loans, mortgages, car financing, or new credit cards. It may also lead to higher interest rates and lower credit limits.

Impact on FICO Score

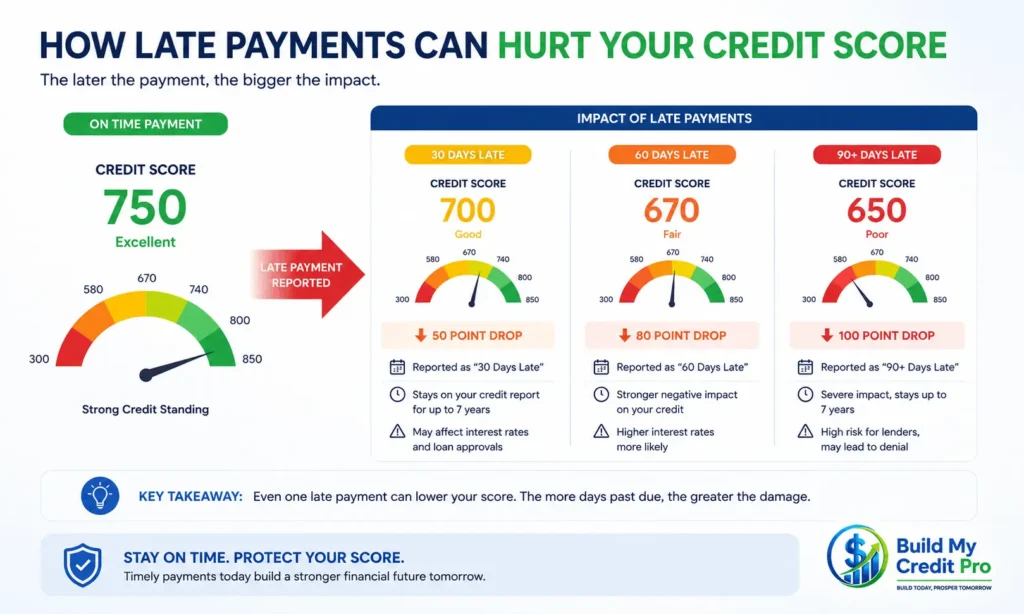

Your payment history makes up about 35% of your FICO score, making it one of the biggest credit score factors.

A late payment can lower your score depending on:

- How late the payment is

- How recent the missed payment is

- Your current credit score

- Your overall credit history

People with higher credit scores often see a larger drop after one late payment because they had a stronger credit profile before the mistake happened.

For example, someone with excellent credit may lose many points after missing a payment, while someone with poor credit may notice a smaller decrease.

This is why many people search for ways to remove late payments from a credit report and improve their credit score quickly.

Difference Between 30-Day, 60-Day, and 90-Day Late Payments

Not every late payment impacts your credit score in the same way, as the effect depends on factors like how late the payment is and your overall credit history. The longer the payment remains unpaid, the more damage it can cause.

| Late Payment Status | Possible Credit Impact |

|---|---|

| 30-day late payment | Moderate negative impact |

| 60-day late payment | Bigger score decrease |

| 90-day late payment | Serious credit damage |

| 120+ days late | High risk of collections or charge-off |

A 30-day late payment is usually the first warning sign for lenders. However, 60-day and 90-day late payments show a more serious payment problem and can remain damaging for years.

If a debt remains unpaid for an extended period, the creditor may transfer the account to a collection agency or mark it as a charge-off on your credit report. This can make rebuilding your credit much harder.

Learning how to remove late payments from your credit report early may help reduce long-term financial damage.

Can One Late Payment Hurt Your Credit?

Yes, even one late payment can hurt your credit score.

Many people believe a single missed payment will not matter, but once it is reported to the credit bureaus, it can affect your credit profile for years.

The impact depends on:

- Your current credit score

- The type of account

- How late the payment becomes

- Whether you quickly bring the account current

If you accidentally miss one payment, acting fast is very important. In some cases, lenders may agree to remove a late payment through a goodwill adjustment if you have a strong history of making payments on time.

In some situations, one late payment may lower your chances of getting approved for loans, apartments, or low interest financing. That is why understanding how to remove late payments from your credit report can help protect your financial future.

Is It Possible to Remove Late Payments From Your Credit Report?

Yes, in some situations you may legally remove late payments from your credit report. However, not every negative mark can be deleted immediately.

The key is understanding whether the information is inaccurate, outdated, unfair, or correctly reported. Credit laws in the USA give consumers important rights to dispute errors and request investigations.

If you want to fix your credit score and remove negative items, it is important to follow legal and honest methods instead of scams that promise instant results.

When Late Payments Can Be Removed

Late payments may sometimes be removed if:

- The information is inaccurate

- The payment was reported incorrectly

- The account does not belong to you

- The lender cannot verify the late payment

- The late payment is older than the legal reporting period

- You receive a goodwill adjustment from the creditor

For example, if your bank account had a technical error or the lender reported the wrong payment date, you may be able to dispute the information successfully.

Many consumers improve their credit score by finding mistakes and learning how to remove late payments from their credit report legally.

When Accurate Late Payments Usually Stay

If the late payment information is accurate and verified, it will usually remain on your credit report for up to 7 years.

Credit bureaus are legally allowed to report accurate negative information during this period. Paying the account helps prevent additional damage, but it does not automatically remove the late payment history.

However, the effect on your credit score becomes smaller over time if you continue building positive credit habits such as:

- Making on-time payments

- Lowering credit card balances

- Avoiding new missed payments

- Keeping older accounts open

Even if accurate late payments cannot always be removed immediately, improving your overall credit behavior can still help raise your credit score over time.

What Rights Do You Have Under the Fair Credit Reporting Act (FCRA)?

The Federal Trade Commission enforces important consumer protection laws, including the Fair Credit Reporting Act (FCRA).

The FCRA gives consumers several important rights, including the ability to:

- Dispute inaccurate information

- Request investigations from credit bureaus

- Receive a free copy of your credit report

- Have unverifiable information removed

- Be informed if negative credit information is used against you

Credit bureaus usually have 30 days to review and respond to disputes. If the lender cannot verify the late payment information, the item may need to be corrected or deleted.

Understanding your rights under the FCRA can help you legally remove errors and improve your financial opportunities in the USA.

How to Remove Late Payments From Your Credit Report

Removing negative marks from your credit history takes time, but many people in the USA have successfully improved their credit by following the right steps. If you want to improve your financial future, learning how to remove late payments from your credit report can help you qualify for better loans, lower interest rates, and stronger credit card offers.

Many late payments happen because of real-life problems like medical emergencies, job loss, family expenses, or simple mistakes. The good news is that some late payments can legally be corrected or removed.

1. Check Your Credit Reports for Errors

The first step to remove late payments from your credit report is carefully checking your credit reports for mistakes.

Many Americans discover errors they never noticed before. Sometimes lenders report the wrong payment date, incorrect balances, or even accounts that do not belong to the consumer.

You should review reports from all three major credit bureaus:

- Equifax

- TransUnion

Look for problems such as:

- Incorrect late payment dates

- Duplicate accounts

- Wrong account balances

- Accounts you never opened

- Payments reported late by mistake

- Old negative items that should already be removed

Real-Life Example

Michael from Texas checked his credit report before applying for a car loan. He noticed a credit card payment was marked 60 days late even though he had paid it on time through automatic payment.

After reviewing his bank statement, he found proof the payment was processed correctly. He disputed the error with the credit bureau, and the late payment was removed a few weeks later. His credit score improved, and he later qualified for a lower car loan interest rate.

This is why regularly checking your reports is one of the best ways to remove late payments from your credit report and protect your credit score.

2. Dispute Incorrect Late Payments

If you find inaccurate information, you can dispute the late payment with the credit bureaus or the creditor reporting it.

This is one of the most effective legal ways to remove late payments from your credit report.

You can submit disputes:

- Online through the credit bureau websites

- By mail using a written dispute letter

- Directly with the lender or creditor

Always include supporting documents such as:

- Bank statements

- Payment receipts

- Account records

- Billing confirmations

- Emails from the lender

The stronger your proof is, the better your chances of success.

Real-Life Example

Sarah from Florida lost 45 points on her credit score after a student loan company incorrectly reported a late payment. She gathered her payment confirmation emails and bank statements, then submitted an online dispute.

About 30 days later, the credit bureau completed its investigation and removed the incorrect late payment from her credit report.

Situations like this show why understanding how to remove late payments from your credit report can make a real difference in your financial life.

3. Request a Goodwill Adjustment

Sometimes the late payment is accurate, but the lender may still agree to remove it as a goodwill adjustment.

This option often works when:

- The missed payment was a one-time mistake

- You usually pay on time

- You experienced financial hardship

- You had a medical emergency

- You recently lost your job or faced temporary difficulties

A goodwill adjustment request is simply a polite letter asking the lender to forgive the late payment because of your history as a responsible customer.

Real-Life Example

Jessica from Ohio missed one credit card payment after spending several weeks in the hospital. She had always made her payments on time before this.

After recovering, she contacted the credit card company and explained the medical emergency. Because of her strong payment history, the lender agreed to remove the late payment as a goodwill adjustment.

Her experience shows that sometimes honest communication and responsibility can help remove late payments from your credit report.

4. Negotiate With the Creditor

If you have older debt or collection accounts, you may be able to negotiate directly with the creditor or collection agency.

You can discuss:

- Payment plans

- Account settlements

- Pay-for-delete agreements

- Removal requests after repayment

Not every creditor agrees to remove negative information, but some may consider it if you repay the debt responsibly.

Always ask for written confirmation before sending money.

Real-Life Example

David from California had an old collection account from a medical bill he forgot to pay during a difficult financial period. After improving his income, he contacted the collection agency and offered to settle the balance.

The agency agreed to update the account after payment, which helped improve his overall credit profile over time.

Learning how to remove late payments from your credit report through negotiation can sometimes help people recover from past financial struggles.

5. Set Up Automatic Payments to Avoid Future Issues

Preventing future late payments is one of the smartest ways to protect your credit score.

Many people miss payments simply because life gets busy. Automatic payments can reduce stress and help you avoid accidental mistakes.

You can automate:

- Credit card payments

- Student loans

- Utility bills

You can also:

- Set payment reminders on your phone

- Use budgeting apps

- Monitor your bank balance regularly

- Pay your bills before the due date to avoid late payments

Real-Life Example

Chris from New York used to forget payment due dates because of his busy work schedule. After being charged late fees twice in a single year, he decided to enroll in automatic payments for all of his monthly bills.

Since then, he has not missed a payment, and his credit score has steadily improved.

Building better financial habits is extremely important if you want long-term credit improvement. Even after you remove late payments from your credit report, maintaining on-time payments is the key to stronger credit and better financial opportunities in the USA.

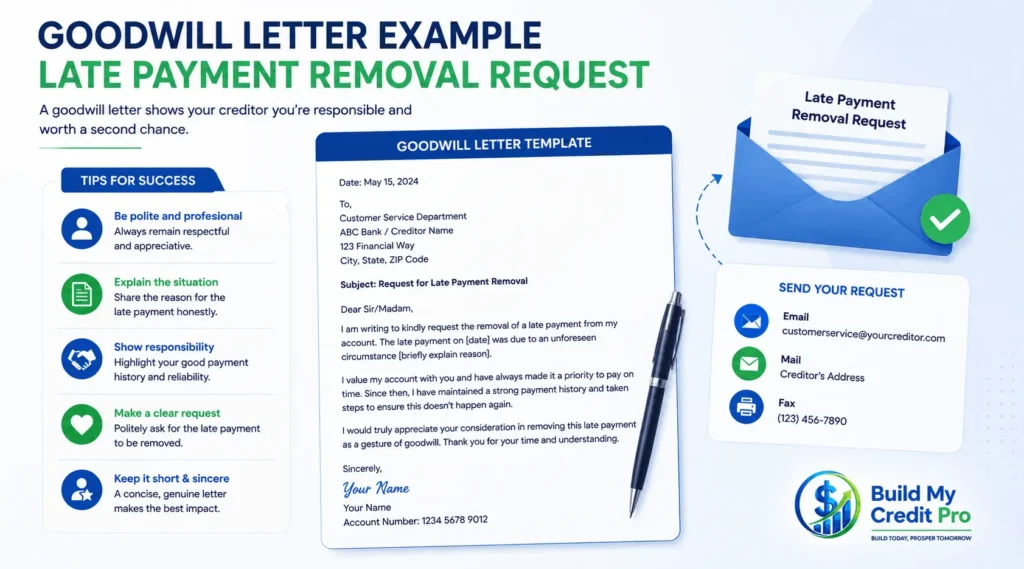

Sample Goodwill Letter for Late Payment Removal

A goodwill letter is one of the most common ways people try to remove late payments from a credit report. While there is no guarantee that a lender will approve your request, many consumers in the USA have successfully received goodwill adjustments after explaining their situation honestly.

This method works best when the late payment was caused by a temporary problem and you normally have a strong payment history.

What to Include in a Goodwill Letter

Your goodwill letter should be polite, professional, and honest. The goal is to show the creditor that the late payment was unusual and that you are now financially responsible.

Include the following details:

- Your full name and account number

- A clear explanation of the situation

- The reason for the late payment

- Proof of responsible payment history

- A polite request to remove the late payment

- Appreciation for their time and consideration

Real-Life Example

Amanda from Arizona missed one payment after her family experienced unexpected medical expenses. She had been a loyal customer for over five years with no previous late payments.

She sent a respectful goodwill letter explaining the situation and asking for understanding. A month later, the lender agreed to remove the late payment from her credit report.

Stories like this show why many people search for legal ways to remove late payments from a credit report and improve their credit score.

Goodwill Letter Template Example

Dear Account Manager,

I hope you are doing well. I am writing to respectfully request a goodwill adjustment for a late payment reported on my account.

The late payment happened during a temporary financial hardship caused by unexpected medical expenses. Before this situation, I always made my payments on time and worked hard to maintain a positive account history.

Since then, I have brought the account current and continued making payments responsibly. I kindly ask if you would consider removing the late payment from my credit report as a gesture of goodwill.

Thank you for your time and understanding. I truly appreciate your consideration.

Sincerely,

[Your Name]

How Long Does It Take to Remove Late Payments?

Many people want fast results after filing disputes or contacting creditors. However, credit repair usually takes time and patience.

The timeline depends on the type of dispute, the creditor, and whether the information can be verified.

Credit Bureau Investigation Timeline

Under the Fair Credit Reporting Act, credit bureaus generally have about 30 days to investigate disputes.

During the investigation, the credit bureau contacts the lender to verify the information. If the creditor cannot confirm the late payment details, the item may be corrected or removed.

Simple disputes may be resolved quickly, while more complicated cases can take longer.

Real-Life Example

Robert from Nevada disputed an incorrect 30-day late payment on his auto loan. He submitted payment confirmations and bank records online.

About three weeks later, the credit bureau completed the investigation and removed the inaccurate late payment from his report.

This is why keeping records and supporting documents is very important when trying to remove late payments from your credit report.

When Credit Scores May Improve

Your credit score may improve shortly after inaccurate late payments are removed. However, every credit profile is different.

Some people notice score improvements within a few weeks, while others may take several months depending on:

- Number of negative items

- Current credit score

- Overall debt levels

- Payment history

Building positive financial habits after the removal is also important for long-term credit improvement.

What If the Late Payment Is Accurate?

Sometimes the late payment information is correct and cannot legally be removed immediately. This can feel frustrating, but it does not mean your financial future is ruined.

Many people in the USA rebuild strong credit scores over time by improving their financial habits consistently.

Even if accurate late payments remain on your report, their impact becomes smaller as time passes and positive information is added.

Ways to Rebuild Credit Over Time

If you cannot remove late payments from your credit report, focus on building new positive credit history.

Helpful strategies include:

- Making all future payments on time

- Paying down debt steadily

- Avoiding unnecessary credit applications

- Keeping older accounts open

- Monitoring your credit reports regularly

Real-Life Example

Kevin from Georgia struggled with missed payments during a period of unemployment. Although the late payments stayed on his report, he slowly rebuilt his credit by paying every bill on time for the next two years.

Over time, his credit score improved enough to qualify for a lower-interest car loan.

This shows that rebuilding credit is possible even after financial mistakes.

Use Secured Credit Cards Responsibly

Using a secured credit card responsibly can help improve your credit history over time.

With a secured card, you usually provide a refundable deposit that becomes your credit limit. Responsible use can help demonstrate positive payment behavior to lenders.

To use secured credit cards wisely:

- Make small purchases

- Pay the balance on time every month

- Avoid maxing out the card

- Keep the account active

Responsible credit card usage can slowly improve your credit profile after late payments.

Keep Credit Utilization Low

Credit utilization means how much of your available credit you are using.

A high utilization ratio can lower your credit score, even if you pay on time.

Experts often recommend keeping utilization below 30%.

For example:

Credit Utilization Ratio = (Credit Used ÷ Total Credit Limit) × 100

Real-Life Example

Lisa from Illinois had a $5,000 credit limit but regularly used over $4,500 each month. Even though she paid on time, her credit score stayed low because her utilization was too high.

After lowering her balances below 30%, her credit score gradually improved.

Managing utilization properly is one of the best long-term strategies after trying to remove late payments from your credit report.

Common Mistakes to Avoid

Many consumers accidentally hurt their credit further while trying to fix it. Avoiding common mistakes can save time, money, and frustration.

Common credit repair mistakes include:

- Filing disputes without proof

- Ignoring collection notices

- Closing old credit accounts unnecessarily

- Applying for too many new credit cards

- Trusting fake credit repair companies

Real-Life Example

Daniel from Michigan paid a large upfront fee to a company that promised to instantly remove all negative items from his credit report. The company stopped responding after receiving payment.

Later, he learned that legitimate credit repair companies cannot legally guarantee instant removals.

Being careful and informed can help protect you from scams while working to improve your credit score.

Should You Use a Credit Repair Company?

Some people choose to hire a credit repair company for help managing disputes and organizing paperwork. Others prefer handling the process themselves.

Both options have advantages and disadvantages.

Pros and Cons of Credit Repair Services

Possible benefits include:

- Help reviewing credit reports

- Assistance preparing disputes

- Educational support

- Time savings

Possible disadvantages include:

- Monthly service fees

- No guaranteed results

- Risk of scams

- Some tasks can be done yourself for free

Many consumers successfully remove late payments from their credit report without paying expensive companies.

Warning Signs of Credit Repair Scams

Be careful of companies that:

- Promise guaranteed credit score increases

- Claim they can remove all negative information

- Ask for large upfront payments

- Tell you to create a new identity

- Advise you to lie on disputes

Legitimate credit improvement takes time and legal steps. Extremely attractive offers can sometimes hide unexpected problems or fees.

The Consumer Financial Protection Bureau warns consumers to research companies carefully before paying for credit repair services.

Best Practices to Protect Your Credit Score

Protecting your credit is much easier than repairing serious damage later. Building good financial habits can help you avoid future late payments and maintain long-term credit health.

Monitor Your Credit Regularly

Checking your credit reports regularly helps you:

- Catch fraud early

- Find reporting errors

- Track score improvements

- Monitor account activity

Many people only review their reports after being denied for credit, but regular monitoring can help prevent bigger problems.

Pay Bills Before the Due Date

Making payments early helps reduce the risk of missed due dates and late fees.

Some people prefer paying bills several days before the official deadline for extra safety.

Real-Life Example

Maria from Colorado started scheduling her credit card payments one week early after accidentally missing a due date during a family vacation.

Since then, she has maintained perfect payment history and improved her credit score steadily.

Simple financial habits practiced consistently can lead to meaningful results over time.

Use Payment Alerts and AutoPay

Payment alerts and AutoPay features can reduce the risk of missing due dates.

Most banks and credit card companies offer:

- Text reminders

- Email notifications

- Mobile app alerts

- Automatic payment options

Using these tools can help you stay organized and avoid future credit problems.

If your goal is long-term financial stability, combining smart payment habits with responsible credit usage is one of the best ways to improve your credit score and reduce the impact of past late payments.

FAQs About Removing Late Payments From Your Credit Report

How can I remove late payments from my credit report?

If you’re wondering how to remove late payments from your credit report, the first step is to verify whether the information is accurate. Errors can be disputed with the credit bureaus, while legitimate late payments may sometimes be removed through a goodwill request to the lender.

Can accurate late payments be removed from a credit report?

Accurate late payments are generally allowed to remain on your credit report. While accurate late payments usually remain on your credit report, some lenders may consider removing them upon request if you’ve consistently managed your account responsibly and the late payment was caused by an exceptional circumstance beyond your control.

How long do late payments affect your credit score?

In the United States, a reported late payment typically stays on your credit history for seven years before it is automatically removed. While their effect on your credit score gradually decreases over time, recent late payments typically have a greater impact than older ones.

What is the fastest way to remove late payments from a credit report?

The fastest way to remove late payments from your credit report is to dispute inaccurate information. If the late payment is valid, you can contact your creditor and request a goodwill adjustment, although approval is never guaranteed.

Does paying off a late account remove the late payment?

No. Paying off an overdue account will bring the account current, but it does not automatically erase the late payment history. The late payment may continue to appear on your credit report for several years.

Can a goodwill letter help remove late payments?

Yes. A goodwill letter is one of the most common methods consumers use when trying to remove late payments from a credit report. In the letter, you explain the reason for the missed payment and politely ask the creditor to consider removing it.

Will removing a late payment improve my credit score?

In many cases, yes. Successfully removing a late payment from your credit report can help improve your credit score, especially if the late payment was recent or one of the few negative marks on your report.

Can late payments stop me from getting approved for credit?

Yes. Lenders often review your payment history when evaluating applications. Removing inaccurate late payments and maintaining positive credit habits can improve your chances of approval.

Final Thoughts

Learning how to remove late payments from your credit report is an important step toward improving your overall financial health. While negative marks can affect your credit score, they do not have to control your long-term financial future. With the right approach, many consumers in the USA successfully recover from past credit mistakes and rebuild stronger credit profiles over time.

Late payment removal may be possible if the information is inaccurate, outdated, or cannot be properly verified. In other situations, improving your credit habits and maintaining consistent on-time payments can gradually reduce the impact of negative items on your report.

Strong credit is built through responsible financial behavior, not quick fixes. Paying bills on time, managing debt carefully, keeping credit utilization low, and monitoring your credit reports regularly can help create long-term financial stability.

If you are working to remove late payments from your credit report, focus on steady progress instead of expecting overnight results. Building better credit requires time, consistent habits, and responsible financial choices. Even small positive changes can help improve your credit score over time and increase your chances of qualifying for better loans, lower interest rates, and stronger financial opportunities.

Most importantly, stay proactive and informed. Understanding your consumer rights, reviewing your credit reports carefully, and addressing problems early can help protect your financial future and reduce unnecessary credit damage.

By following responsible credit practices and maintaining a long-term mindset, you can continue moving toward better financial security and a healthier credit profile.