A low credit score can make it harder to get loans, credit cards, and better financial opportunities in the United States. In this guide on How to Fix Your Credit Fast in USA 2026, you’ll learn how to improve your credit score fast, repair bad credit in the USA, boost your FICO score quickly, and remove credit report errors naturally.

If you want to learn How to Fix Your Credit Fast in USA 2026, remember that real credit repair takes time and smart financial habits. There is no overnight fix for bad credit. The best ways to improve your credit score fast include reducing debt, removing credit report errors, making on-time payments, and following proven credit repair tips in the USA to boost your FICO score quickly.

Learning how to fix your credit fast in USA can help you improve your credit score, lower interest rates, and qualify for better loans and credit cards. The best ways to fix your credit fast in USA include paying bills on time, reducing debt, and correcting credit report errors to build a stronger financial future.

In this guide, you will learn:

- What is considered a bad credit score

- Why credit scores drop

- The fastest ways to repair bad credit

- Common mistakes to avoid

Practical steps Americans can take to improve credit scores legally and safely.

Table of Contents

What Is Considered a Bad Credit Score?

In the United States, lenders commonly use the FICO scoring model to evaluate a person’s creditworthiness. Your credit score is a three-digit rating that shows how well you handle credit and repay borrowed money over time.

Here are the general FICO score ranges:

Credit Score Rating

- 300–579 Poor

- 580–669 Fair

- 670–739 Good

- 740–799 Very Good

- 800+ Excellent

A credit score below 580 is usually considered poor. People in this range may face higher interest rates, loan denials, security deposits, and limited financial opportunities.

A fair score between 580 and 669 may still qualify for some loans or credit cards, but usually with less favorable terms. Once your score reaches the good or very good range, lenders view you as a lower-risk borrower.

Credit scores matter because banks, mortgage lenders, landlords, and even some employers use them to evaluate financial responsibility.

Someone with excellent credit is more likely to receive:

- Lower mortgage rates

- Better auto loan terms

- Higher credit limits

- Premium credit card rewards

- Easier approval for apartments

On the other hand, poor credit can cost thousands of dollars in extra interest payments over time.

Why Your Credit Score Drops?

Understanding why your score decreased is one of the most important steps in learning how to fix your credit fast. Several factors can negatively affect your credit report and lower your score.

Late Payments

Your payment history carries the most weight in major credit scoring models and plays a key role in determining your credit score. Missing even one payment can significantly damage your score, especially if the payment is more than 30 days late.

For example, if your monthly credit card payment is due on the 5th and you fail to pay by the reporting deadline, the lender may report the late payment to the credit bureaus. This negative mark can stay on your credit report for up to seven years.

Late payments can affect:

- Auto loans

- Mortgages

- Personal loans

- Student loans

Setting up automatic payments or reminders can help prevent future mistakes.

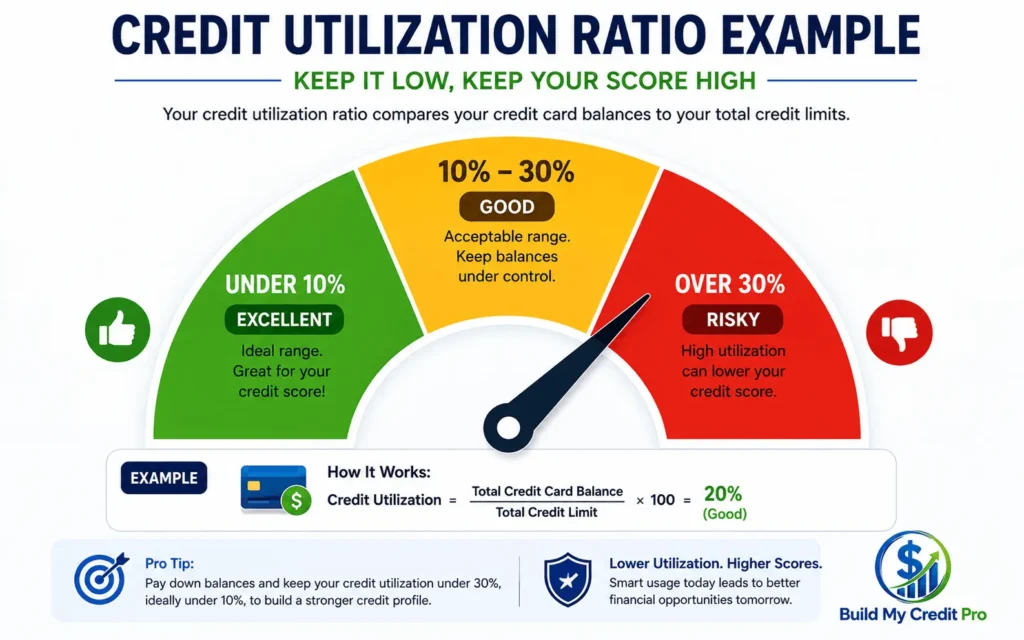

High Credit Utilization

Credit utilization refers to the percentage of your credit card limits that you are actively using at any given time. This factor plays a major role in determining your credit score.

For example:

Credit Utilization Ratio = (Total Credit Used ÷ Total Credit Limit) × 100

If your total credit card limit is $10,000 and your balances equal $8,000, your utilization ratio is 80%, which is considered very high.

Financial experts generally recommend:

- Below 30% = Good

- Below 10% = Excellent

Maxing out credit cards signals financial stress to lenders and can quickly lower your score.

Hard Inquiries

Whenever you apply for new credit, lenders may perform a hard inquiry on your credit report. Too many hard inquiries within a short period can make you appear financially risky.

Examples include:

- Applying for multiple credit cards

- Shopping for personal loans

- Financing a vehicle

- Requesting store credit accounts

One hard inquiry may only reduce your score slightly, but repeated applications can have a larger impact.

Collections Accounts

When unpaid debts are sent to collections agencies, your credit score can drop significantly. Collections accounts tell lenders that you failed to repay a debt according to the original agreement.

Common collections accounts include:

- Medical bills

- Credit card debt

- Utility bills

- Personal loans

For instance, a $200 unpaid medical bill that enters collections can remain on your report for years and negatively affect future loan approvals.

Paying collections accounts or negotiating settlements may help reduce long-term damage.

Maxed-Out Credit Cards

Using nearly all of your available credit can hurt your score, even if you make payments on time.

For example:

- Card limit: $2,000

- Balance: $1,950

This extremely high balance increases your utilization ratio and may signal that you are overdependent on credit.

Many Americans see quick score improvements simply by paying down balances and reducing card usage.

Bankruptcy

Filing for bankruptcy is one of the most serious negative events for a credit report. Although bankruptcy can provide legal debt relief, it severely damages credit scores.

Chapter 7 bankruptcy may remain on your report for up to 10 years, while Chapter 13 typically remains for seven years.

Bankruptcy can make it difficult to:

- Qualify for mortgages

- Obtain low-interest loans

- Open new credit cards

- Rent certain apartments

However, rebuilding credit after bankruptcy is possible through responsible financial management and consistent payment history.Closing Old Accounts

Many people mistakenly believe closing old credit cards will improve their credit score. In reality, closing long-standing accounts can sometimes lower your score.

Older accounts help build your average credit age, which is an important scoring factor. Closing a card may also reduce your total available credit, increasing your utilization ratio.

For example:

- Total credit before closing: $15,000

- Total balance: $3,000

- Utilization: 20%

After closing a card:

- Total credit: $8,000

- Same balance: $3,000

- Utilization: 37.5%

This sudden increase can negatively affect your score.

How to Fix Your Credit Fast

Improving your credit score quickly requires a combination of smart financial habits and consistent action. While there is no instant solution for repairing bad credit, many Americans begin seeing positive changes within a few months when they focus on the right strategies.

The key is understanding which actions have the biggest impact on your credit profile. Payment history, credit utilization, account management, and credit report accuracy all play a major role in determining your score.

Below are some of the most effective and proven ways to fix your credit fast in the USA.

1. Pay All Bills On Time

Your track record of making payments on time has the biggest impact on your overall credit score. In most scoring models, it makes up approximately 35% of your total score. Even one missed payment can significantly damage your credit and remain on your report for years.

Lenders want to see that you consistently pay your financial obligations responsibly. This includes:

- Auto loans

- Mortgages

- Student loans

If you are trying to improve your credit score quickly, making every payment on time should become your top priority.

Many Americans fall behind because they simply forget due dates. Setting up automatic payments through your bank or credit card provider can help avoid accidental late payments. At minimum, always pay the required minimum amount before the due date.

For example, imagine someone misses two credit card payments during a financial emergency. Their score may drop by dozens of points. Once they begin making on-time payments consistently for several months, lenders start seeing positive behavior again, and the score may gradually recover.

Building strong payment habits is one of the fastest long-term ways to repair bad credit.

2. Lower Your Credit Utilization Ratio

Credit utilization is the amount of your available credit that you’re actively using. High balances can quickly hurt your score, even if you make payments on time.

Financial experts generally recommend:

- Keep utilization below 30%

- Ideal utilization is under 10%

Here is the formula lenders use:

Credit Utilization = (Credit Card Balance ÷ Total Credit Limit) × 100

For example:

- Total credit limit: $10,000

- Current balance: $2,000

- Utilization ratio: 20%

This is considered healthy credit usage.

However, if your balance increases to $8,000, your utilization jumps to 80%, which may signal financial stress to lenders.

One of the fastest ways to improve your credit score in 30–60 days is paying down credit card balances. Many people see score increases after lowering utilization because updated balances are reported monthly to credit bureaus.

To lower utilization faster:

- Pay balances before the statement closing date

- Spread purchases across multiple cards

- Avoid maxing out cards

- Make multiple payments during the month

Reducing utilization is often one of the quickest methods to fix your credit fast.

3. Dispute Credit Report Errors

Errors on credit reports happen more often than most Americans think. Incorrect information can unfairly lower your score and make borrowing more difficult.

Common credit report errors include:

- Wrong late payments

- Incorrect balances

- Duplicate accounts

- Fraudulent accounts

- Accounts that do not belong to you

If you notice inaccurate information, you have the legal right to dispute it with the major credit bureaus:

For example, if a credit card company mistakenly reports a late payment that you actually paid on time, that error could hurt your score until corrected.

Start by reviewing your credit reports carefully and gathering proof such as:

- Bank statements

- Payment confirmations

- Loan records

Disputing inaccurate information can sometimes lead to relatively fast score improvements, especially if negative marks are removed successfully.

4. Become an Authorized User

Another smart strategy for improving bad credit is becoming an authorized user on someone else’s credit card account.

This usually works best when:

- The primary cardholder has excellent payment history

- The card has low utilization

- The account has been active for several years

Parents often help adult children build credit this way, but trusted family members may also assist.

For example, if your parent has a credit card with:

- 10 years of positive history

- Low balance usage

- Perfect payment history

Being added as an authorized user may allow some of that positive history to appear on your credit report.

This strategy can help improve:

- Credit age

- Payment history

However, it is important to choose someone financially responsible. If the primary account holder misses payments or carries large balances, your score could also be affected negatively.

5. Avoid Applying for Too Many Credit Cards

When people try to repair bad credit, they sometimes make the mistake of applying for multiple credit cards at once. Unfortunately, this can lower scores even more.

Each application may trigger a hard inquiry, which tells lenders you are seeking additional credit.

A few hard inquiries may only reduce your score slightly, but several applications within a short period can raise concerns about financial instability.

For example:

Applying for five credit cards in one month may appear risky to lenders.

It may reduce approval chances for future loans.

Instead of opening many new accounts, focus on managing your existing credit responsibly.

If you truly need new credit, apply strategically and only when necessary.

6. Ask for a Credit Limit Increase

Requesting a credit limit increase can sometimes help improve your score by lowering your utilization ratio.

For example:

- Current balance: $2,000

- Current limit: $4,000

- Utilization: 50%

If your lender increases your limit to $8,000 while your balance remains the same:

- New utilization: 25%

Lower utilization generally improves your credit profile.

Many credit card issuers allow customers to request increases online. Some companies may even offer automatic increases after demonstrating responsible account management.

Before requesting an increase:

- Ensure payments are current

- Avoid recent missed payments

- Maintain stable income if possible

Keep in mind that some lenders may perform a hard inquiry during the review process.

7. Pay Off Collections Accounts

Collections accounts can seriously damage your credit score and remain on reports for years. Paying them off may not erase all negative impact immediately, but it can improve your overall credit health and reduce lender concerns.

If you have collections debt:

- Contact the collection agency

- Verify the debt is accurate

- Discuss settlement options if needed

Some agencies may agree to accept less than the full balance through a negotiated settlement.

Another strategy people discuss is “pay-for-delete,” where the collection agency agrees to remove the account from your credit report after payment. Still, not every collection agency offers this option, and approval is never guaranteed.

Before paying any collection account:

- Request written confirmation

- Keep payment records

- Avoid verbal-only agreements

Paying collections responsibly can still help demonstrate financial improvement over time.

Fastest Ways to Improve Credit Score in 30–90 Days

While major credit rebuilding takes time, some strategies may produce noticeable improvements within a few months.

Paying Down Credit Card Balances

Lowering balances is often the fastest way to improve your credit score quickly. Because credit card issuers update balances monthly, utilization improvements may appear relatively fast.

Many Americans experience score increases after reducing balances below 30%.

Removing Credit Report Errors

Disputing inaccurate information can lead to faster score improvements if negative items are removed successfully.

For example:

- Incorrect late payments

- Fraudulent accounts

- Duplicate debts

Correcting these errors may quickly improve your credit profile.

Becoming an Authorized User

Joining a family member’s well-managed credit card account may help strengthen your report by adding positive payment history and older account age.

This strategy is especially helpful for individuals with limited credit history or rebuilding credit after financial hardship.

Reporting Rent and Utility Payments

Some modern credit-building services allow consumers to report:

- Rent payments

- Utility bills

- Streaming services

- Phone bills

These payments may not traditionally appear on credit reports, but reporting them can help establish positive financial behavior.

For Americans with limited credit history, adding consistent rent payments may help strengthen credit profiles over time.

How Much Time Does It Usually Take to Improve Your Credit Score?

One of the most common questions Americans ask is, “How long will it take to repair my credit?” The timeline depends on how serious your credit issues are, what negative items appear on your credit report, and how consistently you follow healthy financial habits.

Some credit improvements can happen relatively quickly, while major damage may take months or even years to recover from fully. The good news is that many people begin seeing positive changes sooner than expected once they start taking the right steps.

Here is a general timeline of how long common credit repair actions may take to affect your score:

- Lower credit utilization: About 30 days

- Fix credit report errors: 30–60 days

- Build positive payment history: 3–12 months

- Recover from collections accounts: 6–24 months

Lowering Credit Utilization: Around 30 Days

Reducing your credit card balances is often one of the fastest ways to improve your credit score quickly.

Credit card companies usually report balances to the credit bureaus every month. This means utilization improvements may appear on your credit report within a single billing cycle.

For example:

- Credit limit: $5,000

- Current balance: $4,500

- Utilization: 90%

If you pay the balance down to $1,000:

- New utilization: 20%

A lower credit utilization ratio shows lenders that you manage debt responsibly and can improve your credit score more quickly.

Many Americans trying to fix their credit fast focus on paying down high balances first because utilization has a major influence on credit scores.

Removing Credit Report Errors: 30–60 Days

If your credit report contains inaccurate information, correcting those mistakes may improve your score faster than waiting for negative marks to age naturally.

Examples of common errors include:

- Incorrect late payments

- Duplicate accounts

- Wrong balances

- Fraudulent activity

Once a dispute is submitted, credit bureaus generally investigate within several weeks.

For instance, imagine someone notices a loan incorrectly reported as unpaid even though it was fully paid off years earlier. After providing proof and successfully disputing the error, the negative mark may be removed, potentially increasing the credit score.

Although not every dispute results in removal, correcting legitimate errors can be one of the most effective fast credit repair strategies.

Building Positive Payment History: 3–12 Months

Payment history is the foundation of strong credit. Unfortunately, it also takes time to rebuild after missed payments or financial hardship.

When a person starts paying every bill on time after a history of late payments, lenders slowly begin to see them as a more trustworthy borrower.

For example:

A person misses several payments during unemployment.

After finding stable work again, they make all payments on time for six consecutive months.

Their score may slowly improve as positive history begins outweighing recent negative activity.

While rebuilding payment history requires patience, it remains one of the most powerful ways to repair bad credit fast in the USA over the long term.

Recovering From Collections Accounts: 6–24 Months

Collections accounts can seriously damage a credit score because they indicate unpaid debt obligations.

Recovery time depends on:

- The size of the debt

- Whether the account is paid

- How recent the collection is

- Overall credit habits

For example, someone with multiple unpaid collections may not see immediate improvement after payment, but over time lenders may view paid collections more favorably than unpaid debts.

As collections become older and positive habits continue, scores often begin recovering gradually.

Patience is important here because serious negative marks take longer to heal compared to smaller issues like utilization spikes.

Credit Repair Scams to Avoid

When people feel desperate to improve bad credit, scammers often try to take advantage of them. Many companies advertise unrealistic promises that sound attractive but can actually create bigger financial and legal problems.

Learning to recognize credit repair scams is extremely important when trying to fix your credit fast safely and legally.

FAQs — How to Fix Your Credit Fast in the USA

How can I fix my credit fast in the USA?

Pay down credit card balances, make on-time payments, and dispute credit report errors. Lower credit utilization can improve your score quickly.

How long does it take to improve a credit score?

Many people in the USA see credit score improvement within 30 to 90 days with consistent payments and lower debt balances.

What is the fastest way to raise a credit score?

Reducing credit card utilization below 10% and avoiding late payments are among the fastest ways to boost your credit score.

Can I repair my credit myself?

Yes, you can fix your credit yourself by checking reports, disputing errors, and building positive payment history over time.

Does paying collections improve credit?

Paying collections may help improve your credit profile and looks better to lenders than unpaid debt.

What credit utilization is best?

Keeping credit utilization under 30% is good, but below 10% is ideal for faster credit score growth.

Will closing old credit cards hurt my score?

Yes, closing old cards can reduce credit history and available credit, which may lower your credit score temporarily.

Conclusion

Understanding How to Fix Your Credit Fast in USA 2026 is the first step toward achieving better financial stability and long-term success. Improving your credit score requires patience, smart financial habits, and consistent effort. Paying bills on time, lowering credit card debt, reducing credit utilization, and monitoring your credit report regularly are some of the most effective ways to rebuild bad credit and improve your overall credit health.

If you want to learn How to Fix Your Credit Fast in USA 2026, focusing on responsible debt management and maintaining a strong payment history can make a major difference. Many Americans improve their credit score faster by avoiding late payments, limiting unnecessary credit applications, and keeping credit card balances low.

While there is no instant credit repair solution, following proven strategies for How to Fix Your Credit Fast in USA 2026 can help increase your credit score over time and create better financial opportunities. Strong credit can help you qualify for lower interest rates, better credit cards, mortgage approvals, and improved loan options in the United States.

Remember, rebuilding bad credit is a gradual process, but every smart financial decision helps strengthen your future. By consistently applying the right credit repair tips and focusing on How to Fix Your Credit Fast in USA 2026, you can build healthier financial habits, improve your credit score, and achieve greater financial confidence for years to come.